2014年6月25日時点

The main focus today is the durable goods orders release, but we'll cover today's "final" revision to GDP as well. Manufacturing, especially durables manufacturing, has been one of the non-dark spots for the economy so far this year. (We can't quite call it a bright spot, but it has performed better than the construction or service sectors.)

Data from the Federal Reserve on industrial production show factory output rebounding in the spring enough to more than offset the earlier weakness induced by the polar vortex. In fact, industrial production is the only major economic indicator released by the government where the spring rebound has more than offset winter softness.

A separate, somewhat different take on US manufacturing is provided by the Census Bureau's report on factory orders and shipments. Durables orders is an advance take on that release. They too show a spring rebound, but not so strong as that indicated by industrial production.

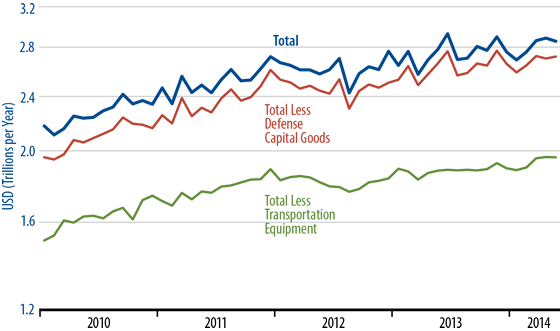

As seen in the chart, durable goods orders show a winter slump and a March rebound, but no change since then. We prefer the measure excluding transportation equipment, because it is less volatile, but all three measures in the chart exhibit essentially the same pattern: the post-winter rebounds bring activity levels back to pre-2014 trend lines, but there has been no above-trend production in spring to offset below-trend winter activity. In sum, however you slice it, average orders for 2014 to date are softer than what we saw in 2013.

We shouldn't overstate the importance of this below-trend-on-average performance for 2014 to date. It is clear that there is no indication in these data of any improvement in factory activity from the sluggish trends of the past 18 months. So, the durable goods data show a less favorable reading on the factory sector than what the industrial production data are now saying. We'll have to wait and see which proves to be the more accurate assessment.

Meanwhile, 1Q14 GDP data were revised downward surprisingly sharply, to -2.9%, from -1.0% a month ago and +0.1% two months ago. Most of this revision was due to erasing the previously estimated stimulus to health care consumption from Obamacare. While the weather-related 1Q14 declines in inventories, goods consumption, and foreign trade should be reversed in 2Q14, the Obamacare-related markdowns will have no offset in 2Q14 data.