All these measures are volatile month-to-month, even with the very volatile transportation/aircraft component excluded. So none of these January gains, by themselves, are conclusive. However, they continue a string of quite a few months of modestly improving orders data.

Consider core capital goods orders in the accompanying chart. After two years of buoyant gains, core capital goods orders swooned in late-2018 and early-2019. However, they have been grudgingly trending upward at least since spring 2019. Underlying trends for durable goods orders in general look similar.

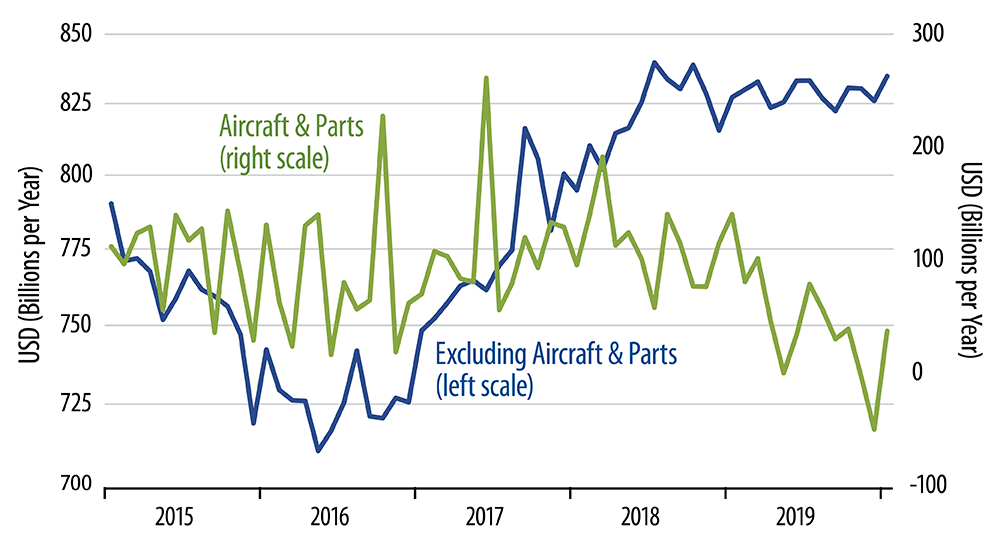

None of these measures are growing as rapidly as one would like. However, none of them are weakening steadily, as would have been suggested by the manufacturing ISM releases announced over the fall. What is more, all these measures are behaving better than they did over 2015-16. And nobody was talking recession then.

Alongside the slightly improving trends of recent months, durable manufacturing has seen a further hit from the prolonged troubles of Boeing’s 737 Max airliner. While aircraft orders have been declining for almost a year, actual production of the 737 declined only in the last month or two, and "upstream" suppliers to Boeing are seeing problems only recently. Given these problems, the recent resilience in durable goods manufacturing activity is actually impressive.

Of course, the January data released today describes activity that took place prior to the recent virulence of the COVID-19 scare. With the risk markets down as sharply in recent days as they have been, it would not be surprising to see a sympathetic "hiccup" lower in CAPEX and durables orders somewhere down the line, say in the March durables data set to be announced in late-April. Hopefully, by the time that news hits the markets, we will have seen some resolution of the virus fears.