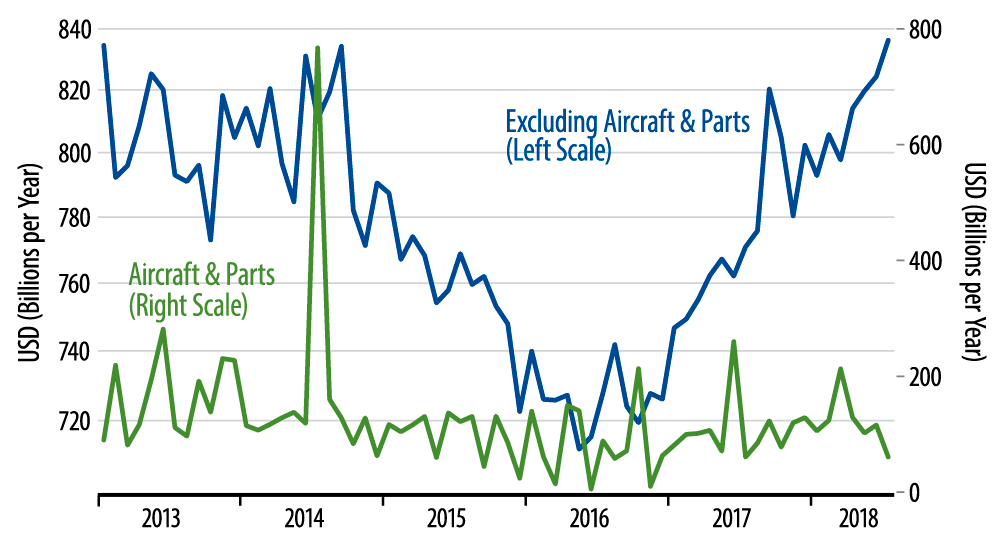

These data show an interesting contrast between developments over manufacturing at large and those within capital goods sectors. Overall durable goods orders have seen slower growth over the last three months, while capital goods orders continued to chug along at a robust growth pace. Thus, since April, durables orders excluding transportation have risen at only a 2.4% annualized rate, compared to 8.0% annualized growth in the preceding 22 months, and headline durables orders have declined over the last three months. In contrast, core capital goods orders have risen at an 11.3% rate, compared to 7.3% growth over the preceding 22 months.

Now, the recently faster growth in capital goods orders has occurred over too small a span to be significant. Still, it is clear that capital goods orders growth has not slowed in the last few months, while overall durable goods orders growth does appear to have slowed. And keep in mind that without the boost from capital goods orders, core durables orders would be down over the last three months.

Part of this disparate movement reflects the boost that the 2017 tax bill provided to business investment ... and part of it may reflect developments in world trade policy, i.e. tariffs. For all the trade bluster coming out of Washington, Beijing, and Brussels, the tariffs we have seen so far have mostly hit "incidental" traded goods and spared trade in more crucial capital goods.

Hopefully, this will continue to be the case. In the meantime, the tilt in manufacturing activity toward capital goods is a favorable one for future growth and productivity prospects. If overall factory activity is going to slow, it is best if that slowing does not affect investment in tomorrow’s economy, and the orders data indicate this to be the case so far.