We have paid special attention to the factory sector in these commentaries. Manufacturing might be a small portion of payrolls jobs, but it is the dominant source of fluctuations in GDP growth, and the recent manufacturing funk has been the dominant factor pulling GDP growth down into the low 1% range over the last year. So, the better news for durable goods orders this morning could be important. The problem is the background context for this news.

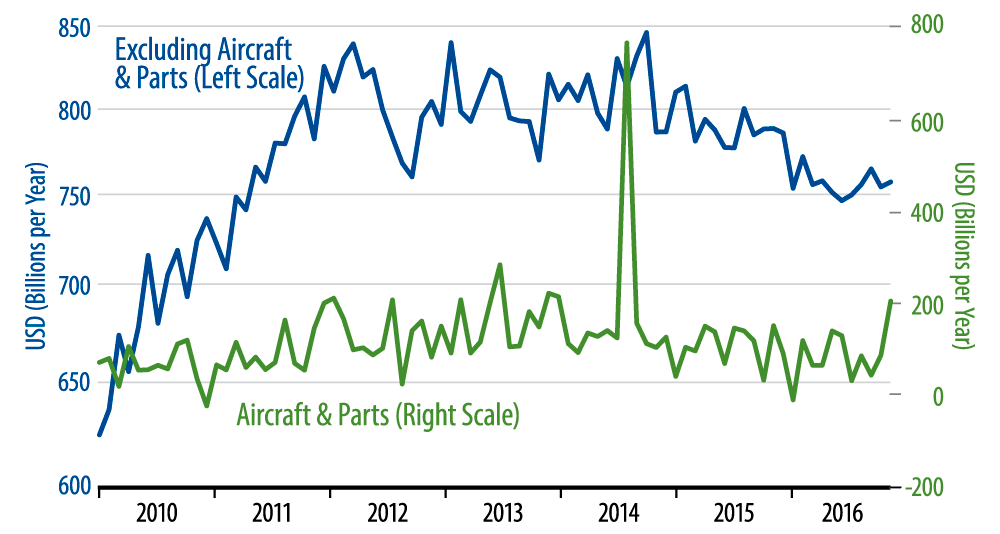

While October durable goods orders look better, previous releases on October factory payrolls and production were especially weak. Similarly, even for durable goods orders, the October gains come on the heels of weaker data in previous months. Thus, as seen in the accompanying chart, the 0.4% October gain in orders for capital goods excluding aircraft (blue line) only partially offsets the 1.4% decline seen in September.

October capital goods orders are above the 2016 lows of July. Still, if you draw a trend line through these data since mid-2014, the “elevated” October level for sales is only slightly above that declining trend. The same goes for durables orders in general. So, maybe factory activity has indeed picked up lately, or maybe it is just one more random fluctuation in the data. (The factory payroll and production data point to the latter.)

The same could even be said of the aircraft orders data. A 138% monthly gain sounds impressive, but as you can see in the chart (green line), even this October swing is within the range of monthly (random) fluctuations over recent years, and aircraft orders have been on a declining trend since 2013.