2015年9月24日時点

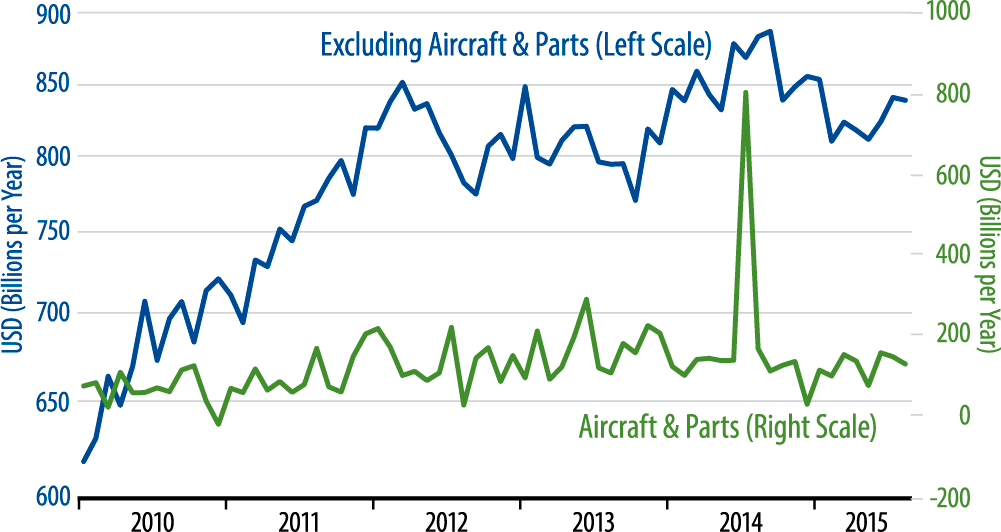

Durable goods orders declined 2.0% in August, and there were modest downward revisions to July data. The headline decline was mostly due to drops in the volatile aircraft orders component. Net of these, orders for durable goods excluding transportation equipment were about unchanged, following a similarly downward revised July number. The durable goods release provides our main monthly information on capital goods activity, and there, orders for capital goods excluding transportation equipment declined 0.2%, with downward revisions to July data as well.

Net of aircraft, the durable goods data were not momentously weak, but the fact remains that US manufacturing activity has been stagnant/declining throughout 2015. Today’s data on August merely confirm the August weakness indicated by earlier reports for factory payrolls and industrial production (85% of which is manufacturing). And, again, the August weakness continues a trend that emerged late last year.

Manufacturing is only about 25% of US GDP, but it is an important 25%, thanks to follow-on effects on shipping, wholesale, and retail activity, and because factory sector swings typically account for about 50% of the swings in GDP growth. The weakening in factory sector activity this year has been a substantial drag on overall growth. Fortunately, that drag has, so far this year at least, been largely offset by a rebound in homebuilding and in construction in general.

However, this combination of weaker manufacturing and stronger construction merely leaves US GDP growth on the same low 2% growth path that we have been mired in for years. While Fed comments have not focused on the factory slide, we believe it is another factor staying its tightening hand. Should the Fed indeed move to try to raise short-term rates late this year, it will do so in a way gauged to have minimal or no impact on term yields, equity prices, or the economy and the fragile factory sector.