US merchandise exports were essentially flat from 2013 through the middle of 2016, helping drive a no-growth environment in US manufacturing. Exports then bounced nicely in late-2016, helping—along with capital spending—revive US factory-sector growth. Since the start of 2017, however, exports have mostly gone flat again, and today’s news for December didn’t really change the picture.

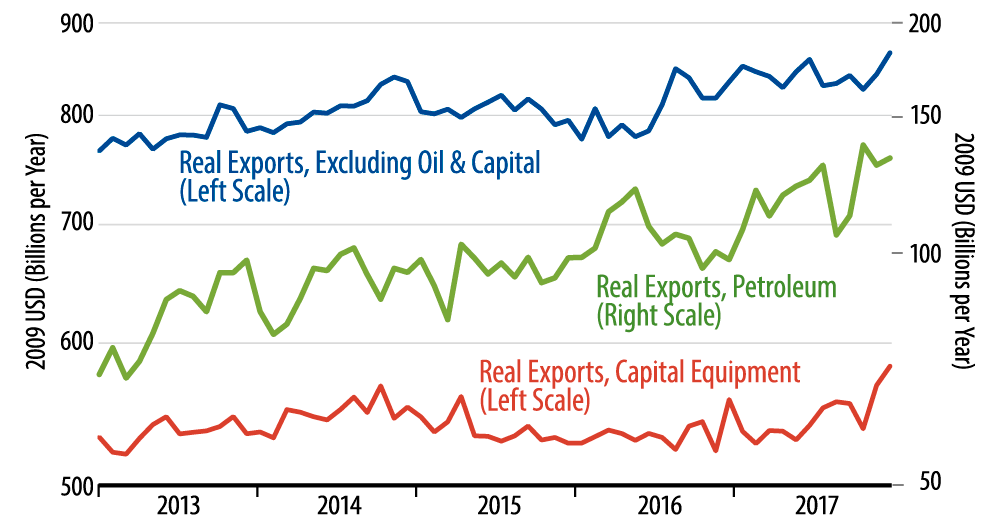

The chart breaks merchandise exports into capital goods (34.5% of all exports), petroleum products (9.1%), and everything else (56.4%). Exports of capital goods failed to bounce with other exports in late-2016, but they have increased over the last six months. Exports of petroleum products have continued to rise nicely for the last two years, reflecting the shale revolution.

For the remaining products, again, after a nice increase in late-2016, we were mostly range-bound throughout 2017. This series does show a bounce in November and December, but even those gains are within the range of the generally flat movement of 2017.

What would cause exports to be flat for three years, then to jump for a few months, then go flat again? That is a great question. With economic growth seeming to perk up globally over the last two years, one would expect a general uptrend in US exports, but that has been hard to find.

In the meantime, US factory-sector growth in 2017 relied on strong growth in capital spending and in inventory investment. The latter looks to have stalled over the last few months. Meanwhile, yes, consumer spending on goods perked up nicely this past Christmas season, but we’ll be surprised if that continues in 2018, given soft growth in personal incomes.

All in all then, we expect only measured growth in US manufacturing in 2018, which is a major reason we remain below consensus in terms of US growth expectations.