Given the February softness in retail sales that we discussed in our March 17 installment of "By the Numbers," it was not surprising that consumer spending on goods was soft. What was surprising was that consumption of services was also soft, showing no growth when swing factors such as utilities and medical care are abstracted from.

This may be an indication of very early consumer response to COVID-19. That is, we expect the virus and its related quarantines to cripple activity in leisure sectors such as travel, accommodations, recreation and food services. The shutdown in these sectors did not start to set in until around March 11, when the NBA suspended play. So, the brunt of these effects should be only partially evident in the March consumption data before becoming fully so in the April data.

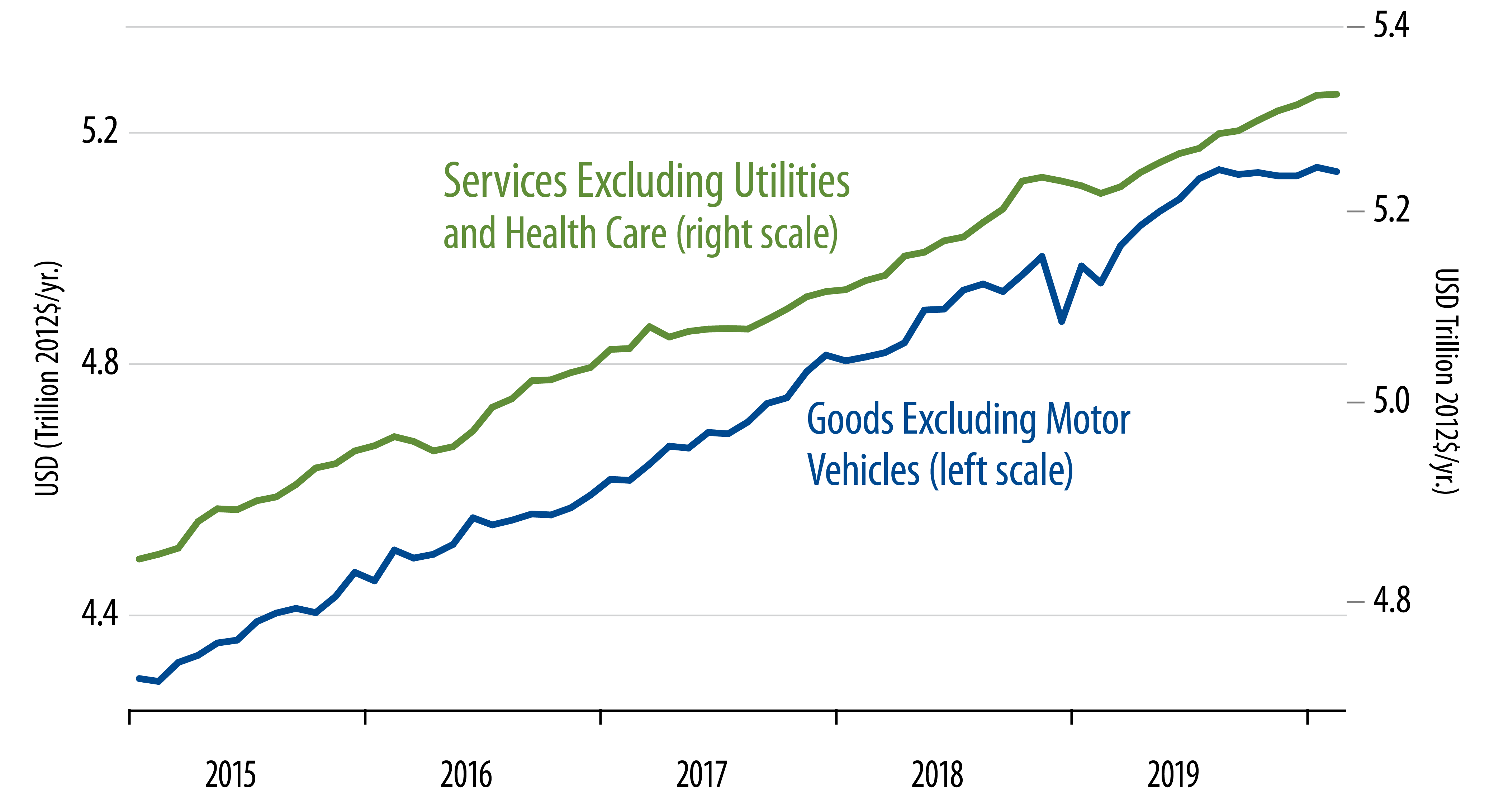

Nevertheless, the February consumption data released today DID show declines in spending in all four leisure sectors listed above. The declines were slight—nothing like what will unfold over the next two months of data. Still, there were declines in all four of these sectors in February, even though most of them had been growing nicely and steadily through the January data. Similarly, underlying services spending in general, as represented by the green line in the accompanying chart, went flat in February, thanks largely to the declines in leisure spending, after it had been growing steadily in preceding months.

Meanwhile, again, personal incomes grew nicely in February, in line with the strong February payroll jobs report released early this month. Households entered the virus episode in as healthy a financial shape as one could hope for, with all measures of income growing at better than a 4% annual clip and saving rates around 8%.

All this will change of course in coming months, as virus-driven layoffs cut into incomes, offset only partially and belatedly by federal government aid. We are hopeful that households’ erstwhile good financial shape will soften the blows from the virus and that at least some sectors can start to reopen before too long. Still, it will be a waiting game in the weeks to come.

Meanwhile, note that next Friday’s jobs report for March also may not show much evidence of virus effects. The payroll job counts reputedly for the whole month of March are actually based on workers employed as of a reference date of March 12, by which time, again, various shutdowns were only starting to occur.