All in all, household incomes look to be growing at an underlying rate of 4%. Take out 1.5% to 2% for inflation, and you have sustained real income growth in the 2% to 2.5% range. This is enough to sustain recent growth rates for consumer spending. It is not enough to drive any acceleration in consumption.

And, indeed, the consumer spending numbers are in accord with this assessment, though there was interesting "context" in today’s spending news. That is, consumer services spending showed some substantial 0.2% upward revisions to 4Q16 data, but February spending data were weak for both goods and services. "Underlying" consumer spending for goods in February rose by less than 0.1%, while spending on services declined a bit more than 0.1%.

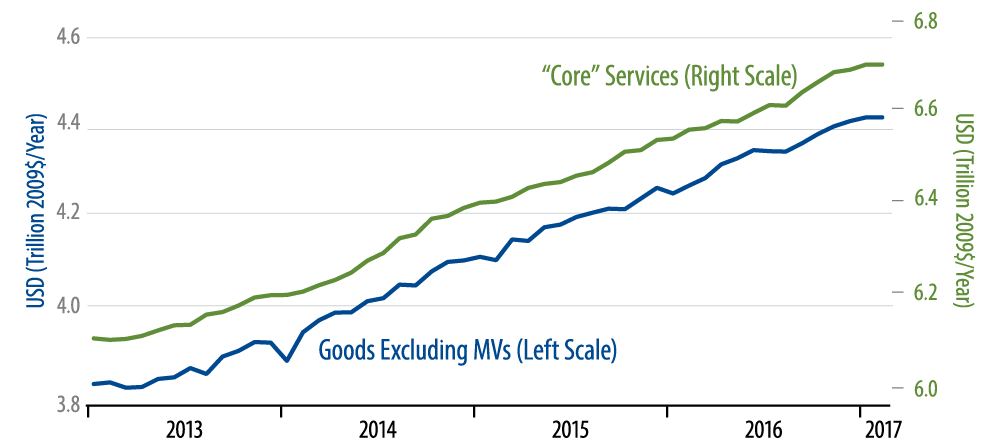

The chart shows goods and service spending excluding the especially volatile vehicles and utilities sectors. Lately, both of these have moved to the downside, reflecting lack of sales incentives and warmer weather, respectively. So, the chart showing total goods and services spending looks similar to this, but with a lot more short-term chop.

Generally, consumption trends look pretty steady. The 1Q17 data to date have been on the soggy side, but this probably reflects random fluctuations more than any meaningful slowing.

The soft January/February spending data will contribute to a lackluster 1Q17 GDP number (we're expecting GDP growth around 1.5%), and the consumer is unlikely to be the propellant of any growth acceleration over the rest of the year. However, neither do we see any meaningful downside risks to growth from the consumer at this point.