The headline data were okay. Total industrial production (IP) rose 0.2% in February, and January’s level was revised up by 0.1%. However, those gains mostly reflect an increase in utilities output, a sector that has been dead flat for years and whose February gains reflect especially cold weather and not an improvement in economic fortunes.

Beneath the headlines, manufacturing output declined by -0.4% in February, and what had originally been announced as a 1.0% gain in December was marked down to 0.6%. Granted, the January level of factory output was not revised lower, but the softer December growth and successive soft gains since then paint a much less favorable picture for manufacturing trends than appeared to be the case a month ago.

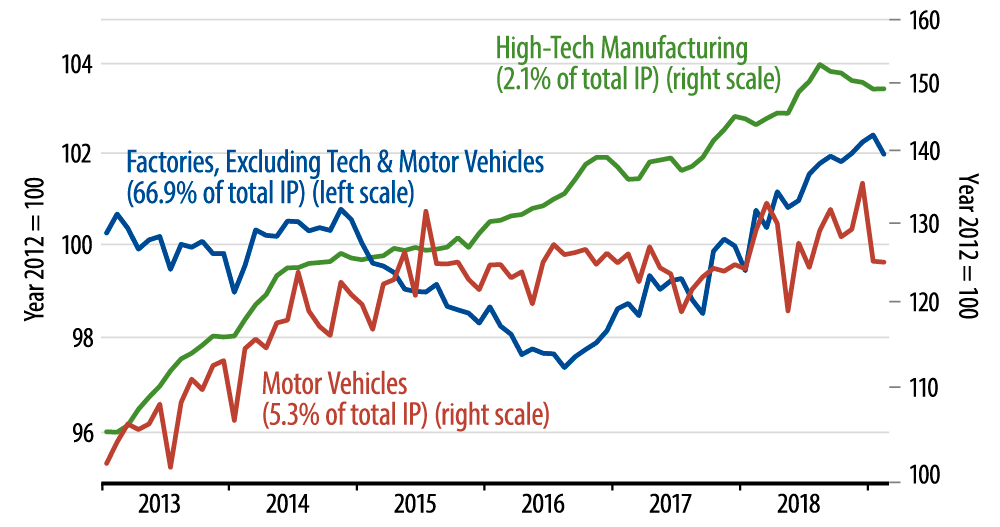

Nor was there any solace in the manufacturing details. High-tech factory output was revised downward especially sharply, followed by essentially no change in February. A month ago, the data portrayed a modest but steady uptrend in tech. Today’s data suggest a declining trend in tech has been in place for six months (green line in chart).

The only upward revisions within factory output came in the motor vehicles industry. And there, as in utilities, the modest improvement does not disguise a desultory trend for more than three years (red line).

In the remaining 90% of the factory sector—and 67% of overall IP—the news was even weaker. There, output fell -0.4% in February, with a -0.1% downward revision to January (blue line). It does not yet look like a declining trend in these "basic" factory sectors. Still, output is unchanged on net over the last five months, and, at best, growth has decelerated substantially in recent months.

As we have commented before, manufacturing and oil production account for ALL of the improvement in GDP growth over the last two years. Both sectors came out of quasi-recession conditions over 2013-16 to rebound smartly starting about August of 2016 through late last year. Today’s data threaten a disruption of those improving trends.

Our baseline case has been that factory output growth would slow some in 2019, as improvements in foreign trade and inventories cooled. Today’s data suggest something more than such a mild slowing.

We always caution not to pay too much attention to any single month’s numbers, and we’ll withhold final judgment here. Still, today’s softness in factory output was presaged by modest softening in factory orders and payrolls, so it is not a completely isolated datum. It serves to "raise the bar" for the factory sector news of coming weeks. We need better data to arrest today’s softness.