2015年03月16日時点

Headline industrial production (IP) rose 0.1% in February, following declines of 0.3% in December and January. The February gain was meager, and even it was overstated by a sharp 7.3% increase in utilities output due to severely cold weather. Net of utilities, IP declined 0.5%.

Now, just as the severe weather boosted utilities output, it probably reduced output elsewhere, just as it likely restrained February retail sales announced last week. However, as was also the case with retail sales, the February declines marked the third straight month of soft readings. So, there certainly appears to be more to the recent softness than just the weather.

This assertion is supported by the fact that measures of factory orders and shipments have also weakened in recent months. All of this squares with the three steps forward, two steps back theme we have cited recently. While the homebuilding data have improved, factory activity has weakened. On net, underlying GDP growth looks to us to be steady, with no sign of the acceleration many are looking for.

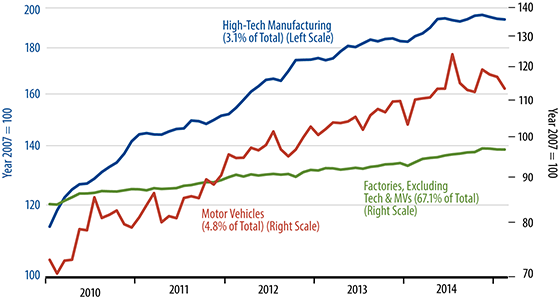

The accompanying chart breaks up manufacturing into high-tech, motor vehicle and low-tech, non-auto sectors. You can see that all three of these sectors have softened over the last three months, a period that begins well before the blizzard set in. In fact, you can see that high-tech manufacturing output ceased growing last summer: the same time that factory orders started weakening.

While high-tech output only comprises 3% of IP, it is also the only major component that has attained pre-recession levels. Finally, data on capacity utilization put high-tech at 67.8%, motor vehicles at 80.0% and low-tech non-auto at 77.7%, all of which are way below levels associated with full utilization of industry resources.