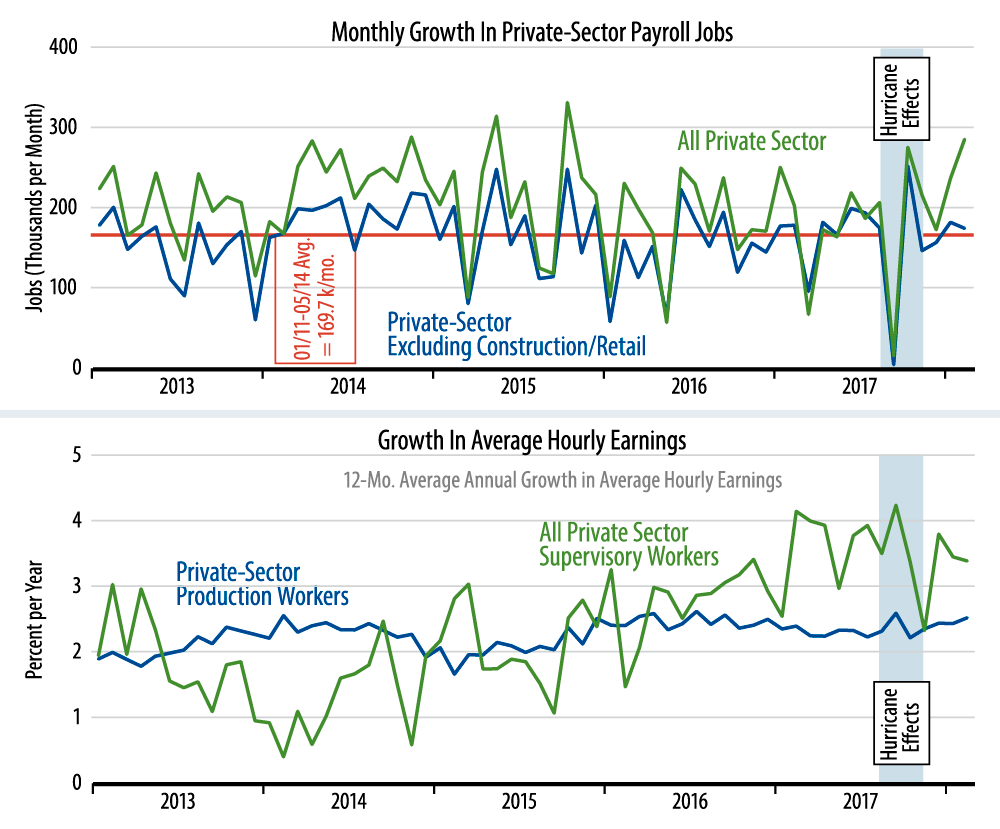

Long-time readers of "By the Numbers" know that we focus on a job measure that excludes the volatile construction and retailing industries, especially around this time of year when both construction and retailing exhibit large seasonal swings. Net of construction and retailing, private-sector jobs rose by 176,000 in February, with a 38,000 upward revision to January.

As seen in the first chart, job growth for this measure is now a bit above its average pace for the last five years, but this follows four months of below-average growth. So, yes, we finally got some decent job growth news this month, but this is the first such positive in a while.

The construction and retailing gains will likely be reversed in coming months, when the seasonals reverse. Meanwhile, on an underlying basis, job growth has slowed markedly in the last three years. Maybe we are indeed at full-employment, but slowing job growth is simply at odds with claims of accelerating economic growth.

Meanwhile we remarked in passing last month that wages "showed a nice increase" in January. Other analysts "bit" harder on the wage gains. Upon examining the data in more detail, even our response looks overdone.

The hourly wage indicator that showed 2.9% yearly growth last month covers all private-sector jobs, even those that don’t get paid by the hour. The government also publishes another measure of hourly wages covering "nonsupervisory" workers only, the 80% of jobs that actually do get paid by the hour. That measure showed a scant 0.1% rise in January, 2.4% year-over-year, with no sign of acceleration.

The news today revised/reversed away most of the gains for supervisory workers, and left nonsupervisory worker wages on a steady growth path. Those claiming wage inflation find no succor in these data.