Retail sales underperformed relative to expectations today, with headline sales down modestly in February (-0.2%) on the heels of a sizable downward revision to January levels (-0.4%) and a modest upward revision to December (+0.2%). Excluding cars, gasoline and building materials, the "control" measure we track rose 0.1% in February, accompanied by a -0.4% revision to January and a +0.2% revision to December.

Just to recap all these changes, headline sales had shown gains of +0.2% in both December and January, and these were revised to +0.3% and -0.4%, respectively, followed by a 0.1% decline in February. Control sales had shown 0.0% in December and +0.4% in January, and these were revised to +0.1% and -0.1%, respectively, followed by a 0.1% gain in February.

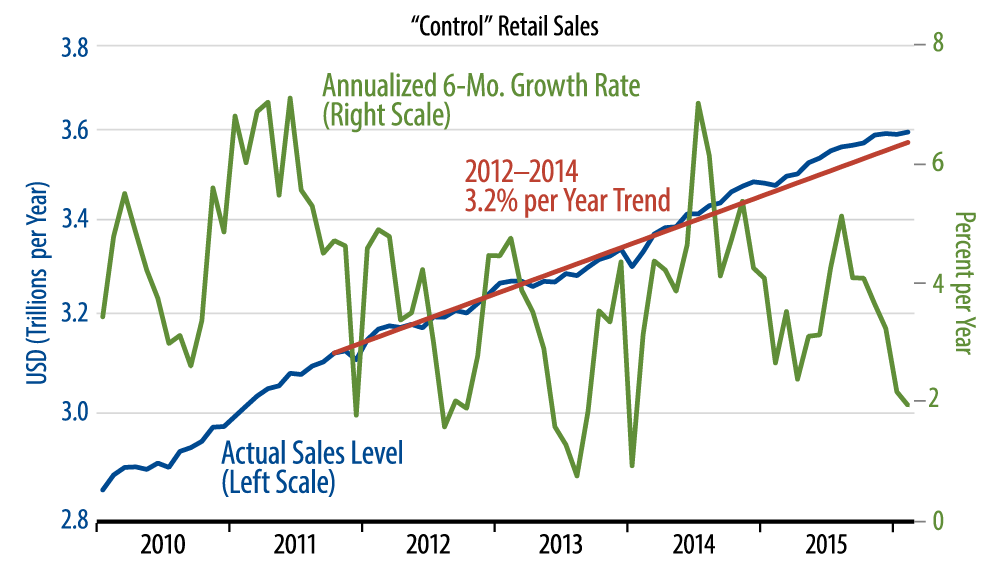

On balance, today's data were softer than expected, but not disastrously so. As seen in the accompanying chart, control sales are essentially back to their 2012-14 trend path, after having moved modestly above trend in mid-2015.

So, this is a blow to those who were looking for stronger consumer spending to buoy economic growth. Our forecast has been for steady consumer growth alongside soft capital spending and exports and a flattening homebuilding sector, aggregating to about 1.5% growth. Today's data are quite consistent with our outlook.

Within sectors, the only really strong component of retail sales was building material stores. Sales declined modestly at motor vehicle dealers, furniture stores and department stores.

One other thing to keep in mind is that each of the last 3 months of sales data feature large seasonal swings that the government statisticians must adjust for, and this is no easy feat. So swings either up or down at this time of year should be approached cautiously. Seasonal swings will be less extreme in the months to come.