Three months ago, a strong November retail sales release ignited hopes for an upswing in consumer spending. Last month, downward revisions and a weak January gain cast doubt on those hopes. Some analysts claimed the consumer upswing was still in place, but was held back by cold January weather. Our take was that the November gains were a Christmas binge and that spending merely reverted to its modest, pre-holiday trend when the Christmas season was over.

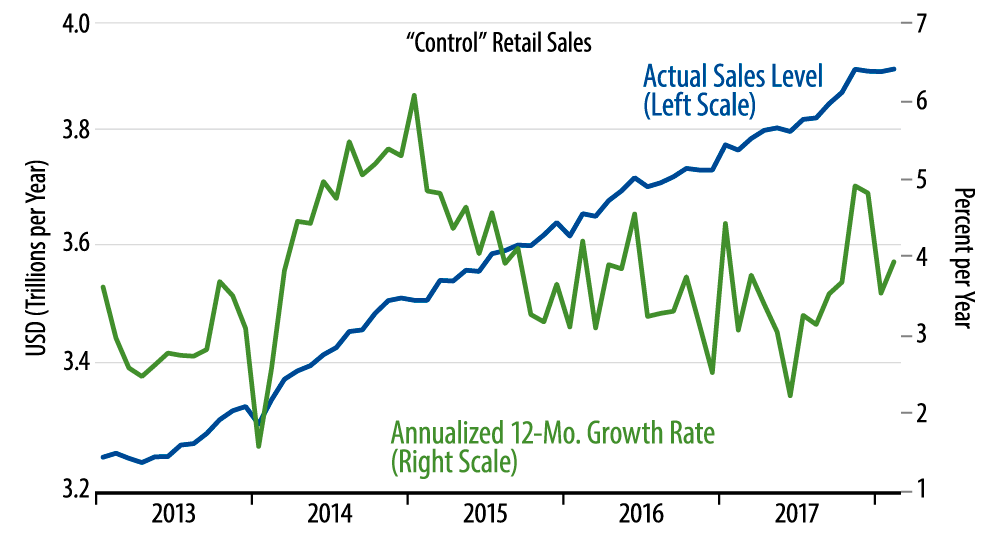

To sustain the upswing story, a strong February sales gain was necessary. Needless to say, we didn’t get it. Consider the chart below. This chart makes clear that it was the November increase in sales that was the anomaly, not the soft changes of the last two months. Once again, that softness merely pulls us back to the same trend line that has been in place for the last three years. The 12-month growth rate in the chart makes the same point.

We thought there was really no reason to expect a consumer upswing in the first place. Growth in gross wage incomes has actually slowed a bit in recent years. Furthermore, unlike most analysts, we were not impressed by the personal tax cuts within the recent tax reform, thinking that the big changes there were all on corporate taxes. So on this count as well, there was no reason to expect a sustained bump in spending. On net, the data of the last four months have been consistent with that story.

In terms of individual store types, the sales data were dreary across the board. The only sector showing decent sales gains was apparel, up 0.4% in February after a 0.9% gain in January, and those gains seem to have been due mostly to price increases there. (The Consumer Price Index for apparel was up 1.5% in February, following a 1.7% increase in January.) Even online (nonstore) retailers showed “only” a 1.0% gain in February, which barely offset a 0.9% decline in January, leaving online retailers just about back on their pre-holiday trend path.