However, today’s February retail sales report rectified only some of the questions concerning the course of the consumer. The February sales data showed general declines, but these were more than offset by sharp upward revisions to January’s sales gains. Meanwhile, previously soft online sales data are now back "on line." On net, both pessimists and optimists on the economy can find something in these data to support their story.

Headline retail sales showed a -0.2% decline in February, but January’s gain was revised to 0.5%, from the previously reported 0.2%. We focus on a measure of "control" sales that excludes cars, gas, and building materials, but includes restaurants. That measure showed a -0.1% decline in February, but a 1.4% gain in January revised upward from the 1.0% initially reported. In other words, across the board, upward revisions to January were larger than the declines reported for February.

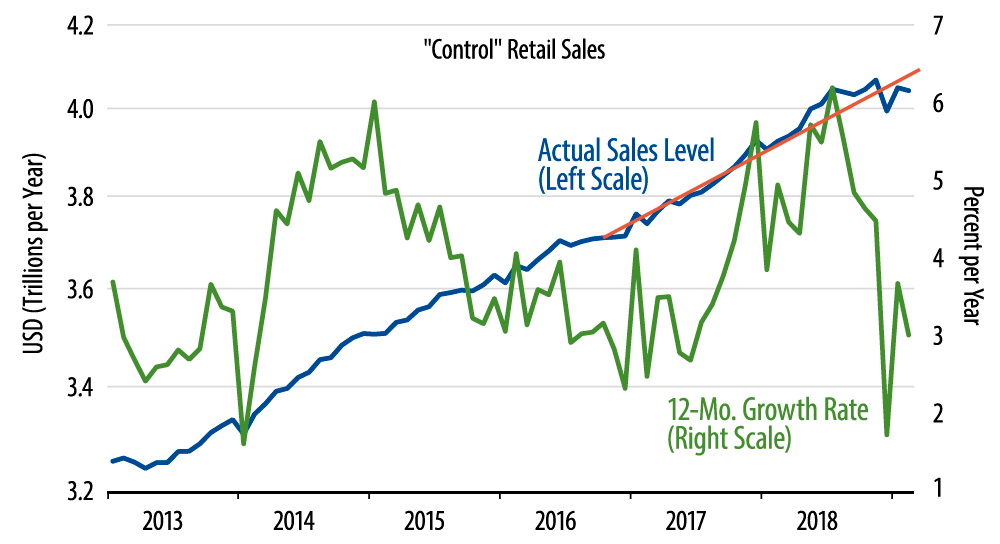

The accompanying chart tells the story. Sales gains last summer and in November had pulled control sales levels above underlying trends. We thought those gains would prove ephemeral, so that sales would move back to those trends (orange line in chart). This is essentially what has happened. Notice that the 12-month growth rate for control sales is right back to 2016-17 norms.

Granted, the February sales decline has pulled sales levels back slightly below "underlying" trends, but only slightly so, and it may be that the vestiges of the Polar Vortex in February worked to restrain February sales. Our guess is that the March sales levels to be announced on April 18 will bring sales levels back to underlying trends. So, we don’t see the recent sales softness as a harbinger of recession—or even of a serious slowing in economic growth—but only the mark of a return to more sustainable trends.

Within store-type details, one of the oddest elements within the soft December sales data was a plunge in sales for online vendors. Today’s data did clear up (reverse) that oddity. With February online vendors showing a 0.9% sales gain on top of a whopping +2.4% upward revision in January—to what is now a 4.5% January gain—online sales are now fully back to their previous, strong growth trends. That December decline in online sales seems to be a hiccup offsetting a run of early holiday shopping by consumers.