For months, the consumer confidence data have been buoyant, causing many to think that consumption was set to accelerate. We even got a taste of strength when November retail sales rose firmly. However, those strong gains were followed by weak growth over the subsequent three months. Today’s data on consumer spending through February show so-so growth for consumption of services as well as of goods.

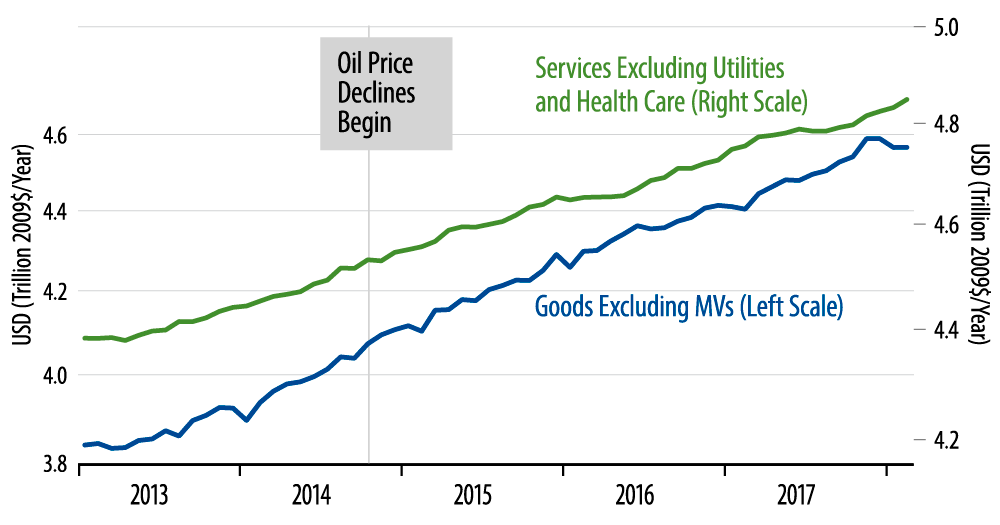

Headline real consumption was essentially unchanged in February (up 0.01%), with a very slight (0.03%) upward revision to the January decline. Both headline goods and services consumption were essentially flat. When one extracts “eccentric” components, such as motor vehicles, utilities and health care, goods consumption remained flat, but services consumption showed a decent 0.3% gain. These “underlying” spending measures are plotted in the accompanying chart.

You may be thinking: “Well, he’s taken out vehicles, utilities and health care, how are those performing?” The answer is: not great. Both vehicles and utilities consumption have declined over recent months. Health care spending is rising, but at a slower rate recently than what we saw in mid-2017.

Apart from these, underlying consumption is back on pre-Xmas trends. We’re not talking actual weakness. There just isn’t any sign of acceleration to support the contention that the economy has improved in recent months.

Personal income did show nice growth in February, in line with the better February jobs data. If job growth continues in the 250,000-plus range, this faster income growth would continue and so would faster consumption. As of now, however, this outcome looks like a tall order.