4Q15 real GDP growth was announced this morning at an anemic 0.7%, pulling average growth for 2015 down to 1.8%. The news was not surprising, as various analysts had projected near-zero numbers, and our own internal model’s forecast was for -0.2%. Nevertheless, it is still a pill that both markets and the Fed will have to swallow. No one knows for sure, but it would be surprising to see the FOMC move to raise short rates again in March on the heels of this, especially given that a hopefully more reassuring print for 1Q16 won’t be forthcoming until the end of April.

With oil prices tumbling and global markets in turmoil, there has already been much talk of recession, and a “zero handle” growth number will likely stoke such speculation. We think such a reaction is inappropriate. The lousy GDP print was in part the product of a series of one-off drags: factors that depressed growth in 4Q15 but that will not recur going forward.

Specifically, with warm weather reducing utilities usage, with a brief lull in motor vehicle production, with some home sale closings delayed due to new mortgage regulations and an odd seasonal (?) plunge in aircraft production, 4Q15 GDP growth would have been a full percentage higher but for these anomalies. It is typical for such isolated factors to distort quarterly numbers a bit. What is unusual is for four major downward anomalies to occur in the same quarter, without any upside anomalies to offset them.

Of course, even a 1.7% growth rate (i.e. net of anomalies) is slower than the pace of recent years. Indeed, we have thought all along that 2016 growth would be disappointingly slow. However, 1.7% growth is not near recession territory, and we believe 2016 growth will settle in at a pace well above the 4Q15 print.

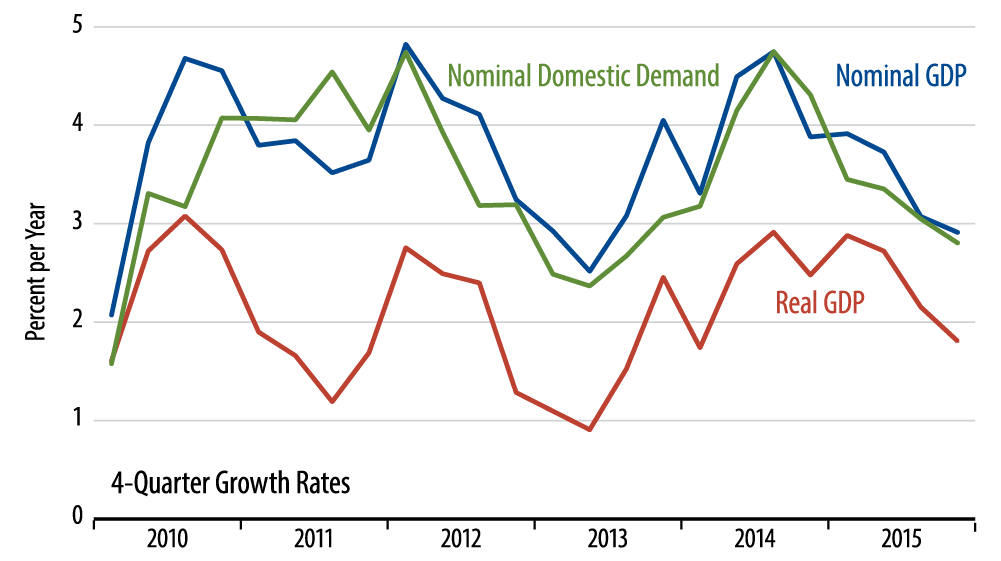

The accompanying chart is a good summary of our take on the economy. US growth is clearly slowing rather than accelerating but the pace is well above zero. Meanwhile, total nominal spending is also slowing, and this is prima facie evidence that inflation will continue to fall below Fed targets.