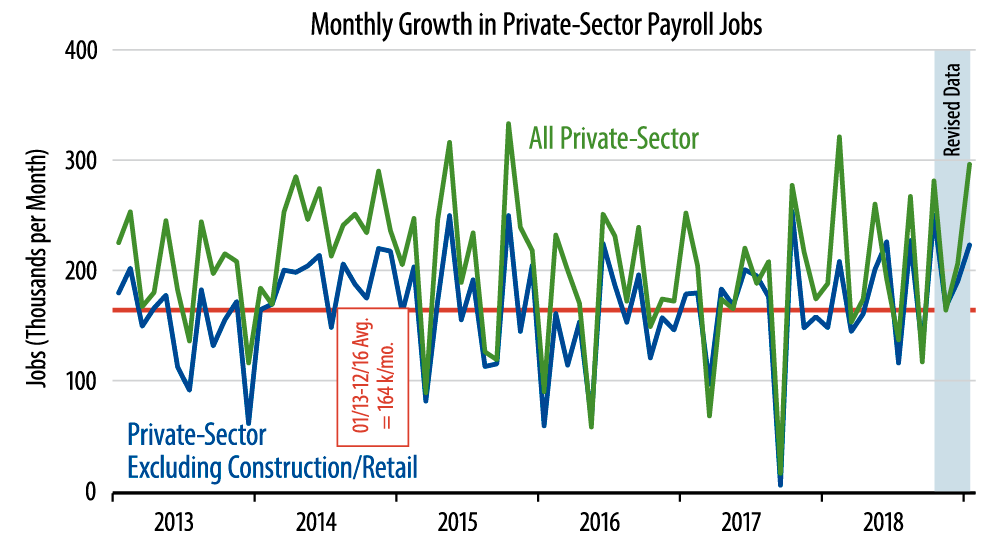

Another factor to consider is that November, December, January, and February are very volatile months seasonally anyway, as the waxing and waning of the holiday season as well as winter weather effects impact the data (seasonal adjustment being a sketchy process). To partially allow for these seasonal vagaries, we focus on private-sector jobs excluding construction and retailing, these two sectors typically being most sensitive to such seasonal vagaries.

Indeed, in today’s January data, we saw construction jobs rise 52,000 and retail jobs rise 21,000, both after seasonal adjustment. Before such adjustment, the respective changes were -265,000 and -558,000. When sectors see such wild ups and down due to the calendar, the "signal" beneath that noise is very hard to detect, and it is likely that warmer than usual early January weather overstated both of these. We’ll see how the polar vortex affects the February data in the other direction.

Bottom line, net of construction and retailing, we saw job gains of 223,000 in January, with a 190,000 revised gain in December. That December gain was previously estimated to be 239,000, and previous data through November saw cumulative benchmark revisions of +23,000.

While these gains are not as impressive as the circa-300,000 gains in headline jobs, keep in mind they come off a lower base. This net of construction and retailing series saw typical gains of 164,000 per month through 2017, so the 223,000 and 190,000 gains reported for the last two months are still well above previous years’ trends.

We have put a lot of emphasis on the manufacturing sector as the dominant source of better economic growth over the past two years, and there, today’s news was not as favorable. Factory payroll jobs through November were revised by a cumulative -20,000, while the December gain was revised from +32,000 to +20,000, and January saw a gain of only 13,000.

Any positive numbers for manufacturing is good news, but today’s data seem to confirm that manufacturing will see somewhat slower growth going forward, thanks to recent slowing in growth in exports and capital spending.

Overall, we see the jobs data as consistent with our 2019 forecast of 2.0%-2.25% GDP growth. The accompanying chart mixes pre-revision data through October with revised data for November through January. So, keep in mind that this chart will look different when we have had a chance to fully fold in revised numbers.