2014年6月17日時点

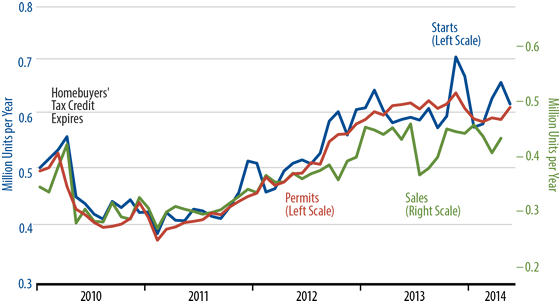

In order for homebuilding to contribute anything to GDP growth, housing-starts levels need to be rising. Such a rising level of housing starts (as well as housing permits and home completions) was in evidence in 2011 and 2012, but homebuilding levels generally have been flat since the end of 2012. This has continued to be the case recently. Yes, we had a spike in single-family starts in late-2013, but that series has since come back to ground, and single-family permits and completions have been steady at best in recent months, with neither of these latter indicators confirming the brief, late-2013 burst in starts.

The accompanying chart provides a good summary of the homebuilding picture. Single-family starts show that late-2013 spike, then weather-depressed declines in January and February, followed by a rebound off the winter lows in the spring months. Average these ups and downs together, and the trend is essentially flat. The same can be said for single-family permits and, finally, for new-home sales.

There is no real evidence of a weakening in homebuilding, but neither is there an indication of a growth trend. So, homebuilding is stuck at what most agree is a weak level of activity, but with no sign of any strengthening. And, as stated at the outset, flat homebuilding means no contribution from housing to any GDP growth, let alone the faster growth that the Federal Reserve and most of the Street are hoping for. Faster GDP growth would require accelerating homebuilding activity, and the existing data do not come close to suggesting that.