Housing starts dropped 2.5% in December, with the crucial single-family starts component down 3.3%. However, both of those declines were completely offset by upward revisions to November data. Thus, the December prints for both total and single-family starts were level with what November starts levels were originally announced at a month ago.

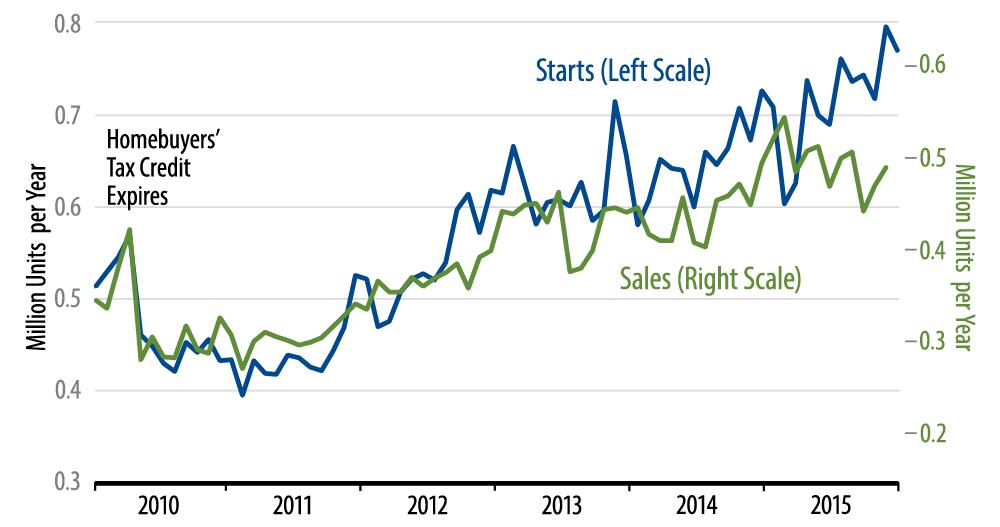

If this “down...but” routine sounds convoluted to you, just look at the accompanying chart showing single-family starts activity (against new-home sales). As the chart makes clear, the December decline is well within the range of “normal” month-to-month fluctuations in starts, and, more to the point, the uptrend in single-family starts that took hold about a year ago looks still to be in place.

Frankly, this is a bit confounding to us. As also seen in the chart, new-home sales have been flat to falling opposite the uptrend in starts. Homebuilders’ inventories of unsold new homes have been rising commensurately and are high relative to sales levels. As a result of this divergence, we have been expecting housing starts to flatten out or even decline slightly, and this caused us to further mark down our 2016 GDP forecast accordingly.

However, as is clear from the chart, such a flattening out in starts has as yet failed to occur, and that is the confounding part. Meanwhile, multi-family starts and permits also continue to plot a volatile but upward-sloping path.

So, for now, homebuilding continues on the rise, a rare bit of good news (alongside job growth) in what has otherwise been a soggy finish to 2015 for the economy. If homebuilding does indeed go flat opposite ongoing woes in manufacturing, this would likely be sufficient to pull US economic growth in 2016 to around 1.5%. For now, though, homebuilding continues to eke out gains, consistent with growth rates a bit shy of 2.0%.