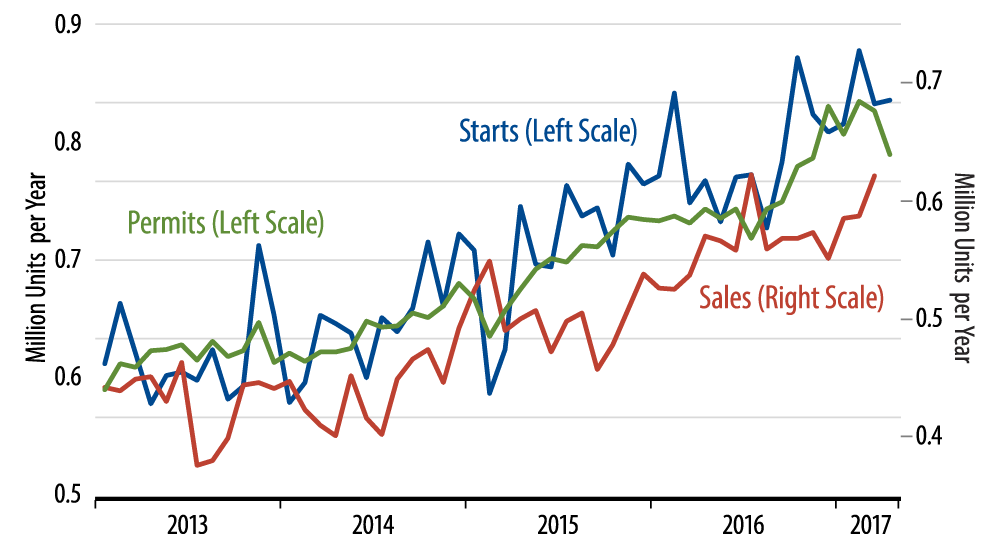

That homebuilding has been able to sustain these elevated levels has been a surprise to us. Last fall, we thought that with household formation so slow and with sales of new homes not high enough to justify the starts increase (compare the blue and red lines in the chart), homebuilding was due for a pullback. Instead, it has stubbornly sustained the gains of last October, and, in turn, homebuilding has provided a nice boost to GDP growth in both 4Q16 and 1Q17.

Going forward, however, the story is mixed. While housing starts have sustained their highs, they haven’t “built” upon those highs, and early-2017 single-family construction spending levels have now caught up with current starts levels. In other words, unless starts show further gains very soon, homebuilding will cease to provide any oomph to GDP growth for the rest of the year.

Meanwhile, multi-family construction has been merely holding steady for the last three years. It continued this steady but volatile path in the April data.

The good news side is that there are no downside risks in the current homebuilding data. The not-so-good news is that we won’t have any more upside risk for homebuilding unless and until housing starts jump further. And as far as contributions to GDP growth go, it is a what-have-you-done-for-me-lately world.