Suppose our team’s star pitcher notches a perfect game, retiring all 27 batters he faces, and next time out he logs a two-hit shutout. Yes, his performance has dropped off from one game to another, but that is only to be expected coming off a perfect game, after which there is nowhere to go but down.

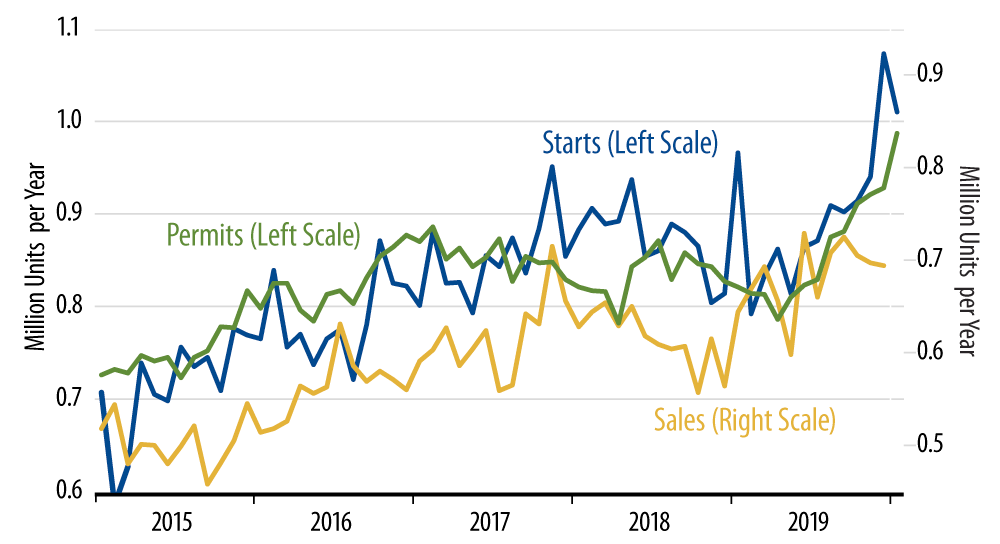

Look at the accompanying chart of single-family starts, permits and sales, and you can see that the January decline is much like the aforementioned pitcher’s performance. The December starts rate of 1.07 million per year was way higher than anything we have seen since the onset of the financial crisis. It would have been literally off the chart, except that we expanded the range of the chart to "hold" it.

Coming off that virtually stratospheric rate, it was highly likely that January would see some decline. Even with the -5.9% reported move, the January starts rate of 1.01 million per year is still higher than anything we have seen in more than a decade.

So, sorry to belabor the point, but even with an apparently substantial decline, January housing activity could still be said to have been really really strong. In fact, it is likely that seasonal factors have been overstating housing activity in each of the last two months.

Before seasonal adjustment, housing activity should be (seasonally) soft in December and January. However, the relatively mild winter across the eastern US has probably served to induce less of a seasonal decline in homebuilding during that period than would normally occur. This then morphs into substantial increases in the seasonally adjusted data, hence the really really high starts rates over the last two months.

Meanwhile, as you can see in the chart, single-family permits have increased in each of the last nine months, to the point that they are almost matching the rate of home starts. Homebuilders are clearly feeling good about things this winter. Judging from our chart, while sales of new homes have perked up substantially over the last year, that rate is going to have to rise sharply further in the months to come to validate the recent pace of housing starts. Either sales will pick up, or else the recent pace of starts will indeed turn out to be a seasonal blip, and spring/summer starts rates will fall back to a pace more consistent with recent sales rates.

Even that latter outcome would still be a relatively benign one for the housing sector. In other data, we have seen some presumably passing problems recently. Retail sales appear to have been held down by a lack of goods coming from China. Manufacturing output has been held back by problems with the 737 Max. Tourist activity is being depressed by fallout from the coronavirus.

In contrast, in homebuilding, we are seeing an embarrassment of riches, with recent activity rates zooming literally off the charts to the upside. Don’t worry about the reported January declines in starts—don’t even worry if we see additional declines of up to 10% over the next few months. That would still leave starts at strong levels.