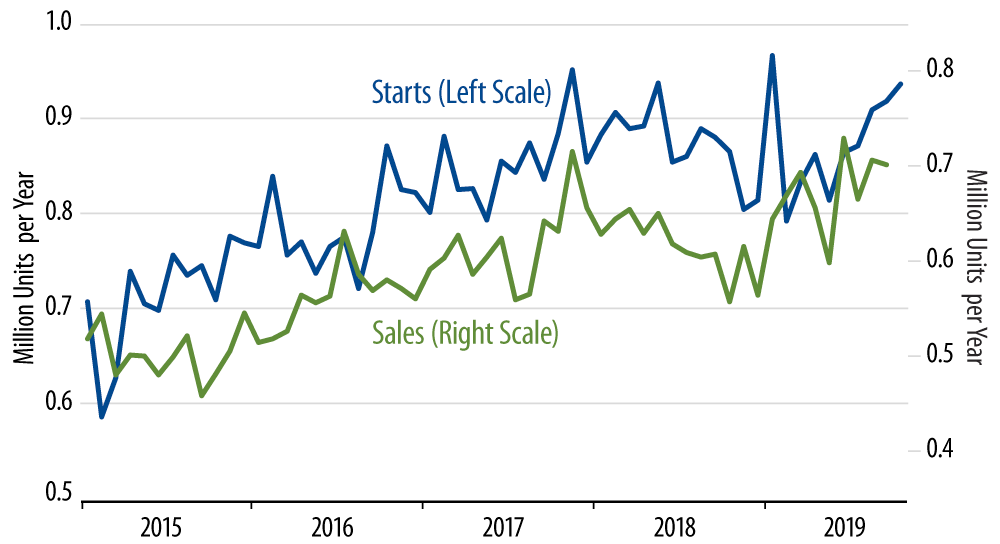

The October level for single-family starts is not quite an expansion high. As you can see in the accompanying chart, we saw starts reach these levels and higher in November 2017, May 2018 and January 2019. However, in each of these three previous cases, the high levels of sales were one-month blips, coming off much lower levels a month earlier and then falling back sharply in subsequent months.

So, the October re-attainment of these highs looks like a more sustainable development, with recent gains much milder and more sustained ... and with sales levels of new homes more closely attuned with starts levels than appeared to be the case when single-starts previously attained these highs.

The late-2019 bounce in single-family starts has certainly been a surprise to us. We expected homebuilding to continue to languish through the end of 2019, as builders struggled to get high levels of unsold new-home inventories under control. Instead, builders have been able to boost home sales via pricing incentives and have ploughed through with further increases on construction levels.

Inventories of unsold new homes still look high to us, nearly six months’ worth of sales, compared to normal inventory levels of four months’ worth of sales. However, new-home demand has held up well, and, again, homebuilders have not skipped a beat in pushing construction levels still higher. Homebuilding was a noticeably positive contributor to 3Q19 GDP growth, and it looks likely to provide a similarly positive contribution in 4Q19.

The regional starts data were similarly encouraging. The South provides nearly 60% of US new-home construction, and starts there were especially strong in October, increasing by 3.0% on top of a 5.0% gain in September and nearing the January 2019 expansion high, also a one-month blip that was reversed in February. The present gains look more sustainable. If you are looking for signs of weakness, you are not going to find them in the homebuilding market.