January durable goods orders beat expectations. Total durable goods orders rose 4.9% in January, about offsetting a revised -4.6% in December. Durables orders excluding the volatile transportation equipment sector rose 1.8%, netting a slight gain over -0.5% and -0.7% changes in November and December. Following suit, capital goods orders excluding aircraft rose 3.9% in January, about offsetting a -3.7% swing in December.

It is clear from this litany that manufacturing has fluctuated around an essentially no-growth trend in recent months. In our below-consensus growth forecast, we have made much of the "stumble" in US factory-sector growth over the past year, and it looks as though that stumble is continuing. At one end of the spectrum, various analysts have largely dismissed the factory sector’s troubles, claiming manufacturing is now only a small portion of the economy and preferring to focus on better-performing consumer and labor market data. At the other end of the spectrum, some analysts lament a "manufacturing recession" and claim that it will pull the aggregate economy down as well.

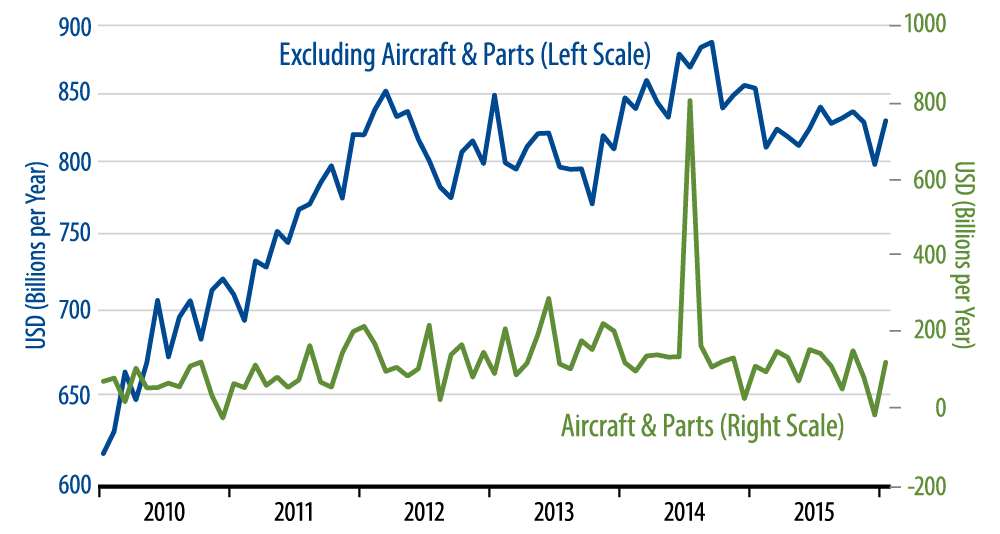

We think both extremes are mistaken. While its share of the economy has declined, US manufacturing is much more volatile than other sectors, and so it accounts for a much larger share of the swings in aggregate GDP growth than its share of GDP might suggest. Meanwhile, factory sector growth has clearly downshifted significantly, but its trends are more no-growth than a recession, as the accompanying chart for capital goods orders attests. (A chart of durable goods orders shows trends similar to those for capital goods.)

So, in a nutshell, January factory news was better. It was not better enough to reverse the sluggish manufacturing trends of the last few years, but it should be sufficient to dispel, at least for now, the recession fears that have surfaced.