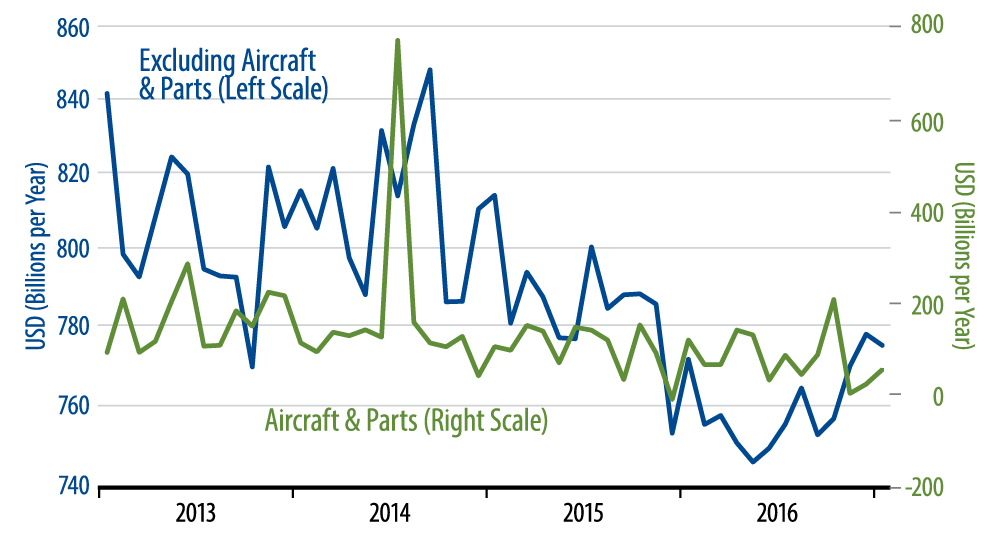

Both durables orders in general and capital goods orders specifically had been trending flat to downward since early-2013, so the recent rebounds are a potentially important signal for US economic growth. Our own view has been that US growth would continue to fall short of investor—and Fed—expectations, largely because we expected continued torpor in US manufacturing activity. Instead, however, virtually all measures of factory activity have shown some rebound over the last few months, with factory orders bouncing first and then manufacturing industrial production showing a bounce with last week's January release.

The only remaining stickler among manufacturing indicators is production hours worked, a component of the payrolls release. Even here, it is no surprise to see order and production data improve before the payroll data do, and we'll see next week whether the February data for factory payrolls finally begin to reflect the marked improvement already seen in other factory indicators.

Our take has been that the 2012–16 softness in factory activity was driven by softness in capital spending and exports. Both have bounced in the last few months, and we'll continue to monitor both to see whether the nascent manufacturing upturn continues. If so, that will be enough to pull US GDP growth up to the 2.0%–2.5% range, compared to the 1.0%–1.5% range numbers we saw a year ago. That, in turn, would likely be enough to keep the Fed on pace for three rate hikes this year.