While last month's job gains were stunning, they left average 2015 job growth just in line with previous years. In other words, the strong late-2015 job gains merely offset softer gains earlier in the year. Well, today's news returned the favor, with soft January gains serving to offset the strong late-2015 data.

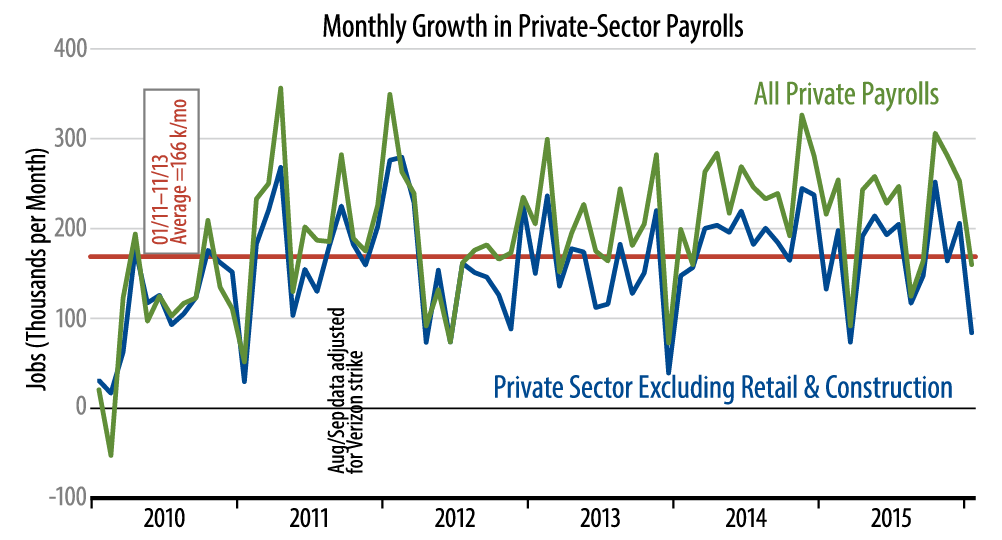

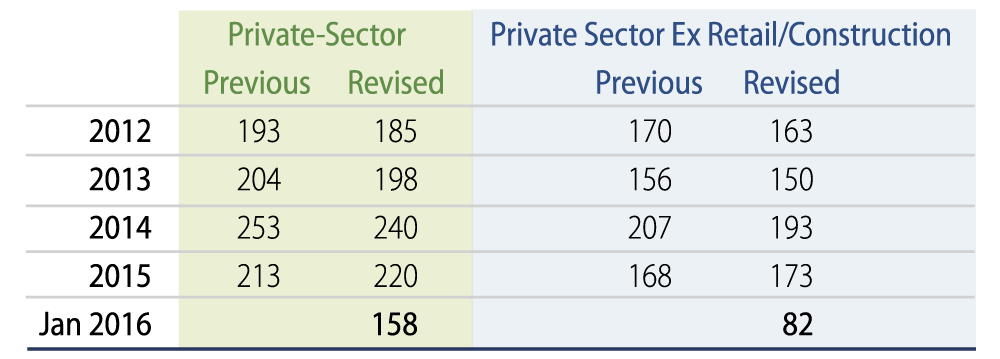

Private-sector jobs rose by only 158,000 in January, with December’s gain revised from 275,000 to 251,000 and November's from 240,000 to 279,000. For the job measure we track most closely, private-sector excluding construction and retailing, January gains were 82,000, with December gains revised from 226,000 to 204,000 and November gains from 160,000 to 162,000. These last gains-excluding construction and retailing-should be compared with a 166,000 monthly average over recent years.

January jobs data are subject to extreme seasonal swings. Before seasonal adjustment, this January's private-sector swing of +158,000 jobs was actually a seasonal decline of -2,475,000, due to various winter shutdowns. The job market then seasonally recoups those losses over February, March, and April. Also, sectors such as retailing are shutting down Christmas-holiday operations in January, creating a seasonal spin all their own.

The bottom line is that it is chancy to draw any hard conclusions from either the January softness in jobs gains or the late-2015 strength. As remarked above, job growth for all of 2015 was about average for this expansion, and 2016 will likely show more of the same. While the January data were below average, seasonal factors might be at work here.

Meanwhile, the Department of Labor also published major revisions of the payroll data back a number of years. As seen in the table, job growth was revised down by about 9,000 jobs per month on average over 2012-14 and up by 7,000 jobs per month on average over 2015.

One surprise in today's news was a large, 29,000 gain in factory jobs. Our guess is that this too is a seasonal blip. Before seasonal adjustment, factory jobs declined 66,000. We'll know more when future months' data come in.