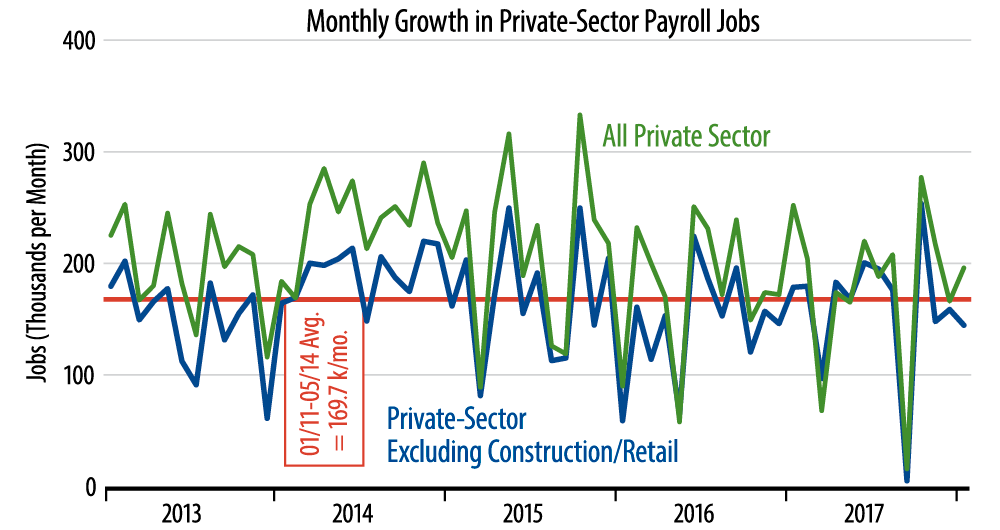

Previous data had shown brisk gains in November and sluggish gains in December. Today’s revisions reversed the order of that sequence, marking November gains down by 38,000 and December up by 22,000. Underneath all the sound and fury, the accompanying chart shows the basic picture.

As we have remarked in previous By the Numbers installments, job growth has generally slowed over the last two years after peaking in 2014-15. Recent data essentially continue that trend. As you can see, when you average out hurricane-depressed September gains (only 5,000) with the post-hurricane rebound in October (254,000), the cumulative increase is well below previous average growth, and the three months since then have all come in below trend as well.

The common assertion is that the economy is at full employment and that this is as fast a job growth rate as we can handle. Even if that is true, the other part of the “common assertion” is that US growth is somehow accelerating. And full employment or not, slowing job growth just doesn’t jibe with claims of accelerating growth.

Meanwhile it should be noted that today’s data featured benchmark revisions to job growth going back a few years. For the data through October, private-sector jobs were revised up by 249,000, while our core measure was revised up by 146,000. It is nice to see upward revisions, after the somewhat larger downward benchmark revisions a year ago, but these stronger gains spread over a couple years don’t move the needle, as can be seen in the chart, which reflects all these revisions.