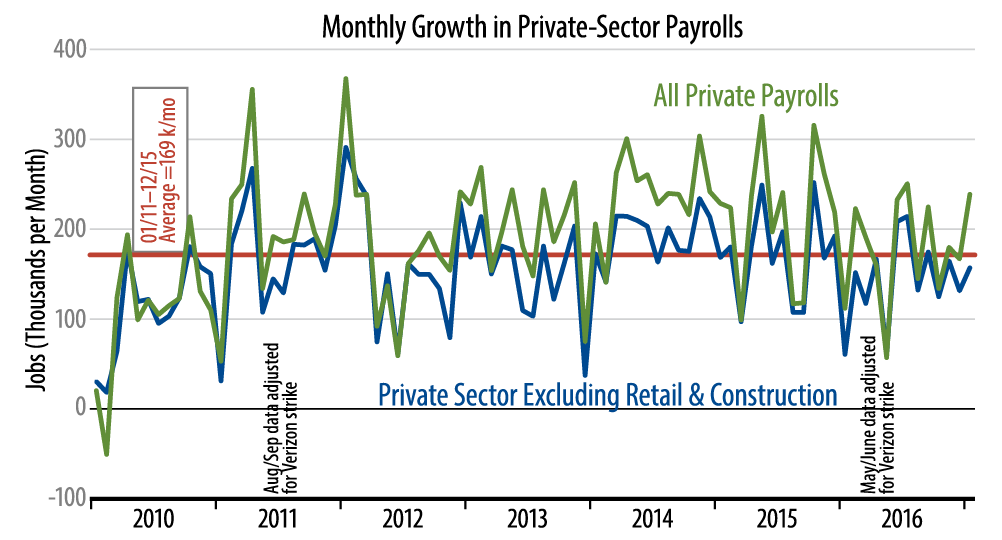

This core measure is not something we made up for this month's data. As regular readers of this column know, we have tracked this particular series month in and month out for years. We exclude retailing and construction not because they don’t matter, but because they typically display wild monthly swings reflecting seasonal anomalies in the retailing and construction industries. Such swings are especially prevalent around year-end, due to holiday season and winter weather issues, so our core measure is especially relevant for this month's data.

The chart tells the story. Underlying job gains have been below prior years' trends for most of 2016 and for four of the last five months of 2016; they continued below those trends in January.

But are mediocre job gains elsewhere being offset by a sudden surge in retailing and construction? Not quite. While retailing and construction saw nice gains in January, 46,000 and 36,000 respectively, those mini-spikes offset relatively soft performance in both series in previous months. Essentially, the "normal" hiring patterns for these sectors have shifted, with less hiring over October–December offset by fewer layoffs in January. (Before seasonal adjustment, construction lost 241,000 jobs and retailing lost 546,000 jobs.) As the government's seasonal adjustment patterns are geared toward past years' developments, these changes show up in the seasonally adjusted data as weakness in October–December and sudden strength in January. On an ongoing basis, both sectors are showing generally steady trends, actually with a bit of slowing in construction sector job growth on average over the last 10 months.

So, yes, the extraneous details of the report were disappointing, with workweeks flat and hourly wages soft. But even apart from that, the job gains for January were not really as buoyant as the media hype would suggest.