Today’s data showed good gains in retail sales beneath the headline data, but there were downward revisions to December. On net, sales trends look better than they did a month ago, but noticeably softer than was the case after the initial November read. Then again, it is possible that January data were held down by the effects of another polar vortex hitting the East Coast.

Headline retail sales rose 0.4% in January, though a -0.5% revision to December left the January sales level 0.1% slightly below the December level estimated a month ago. Our "control" measure excludes sales at car dealers, building material stores and service stations. It showed a nice 1.0% gain in January, only partially offset by a -0.4% revision to the December level.

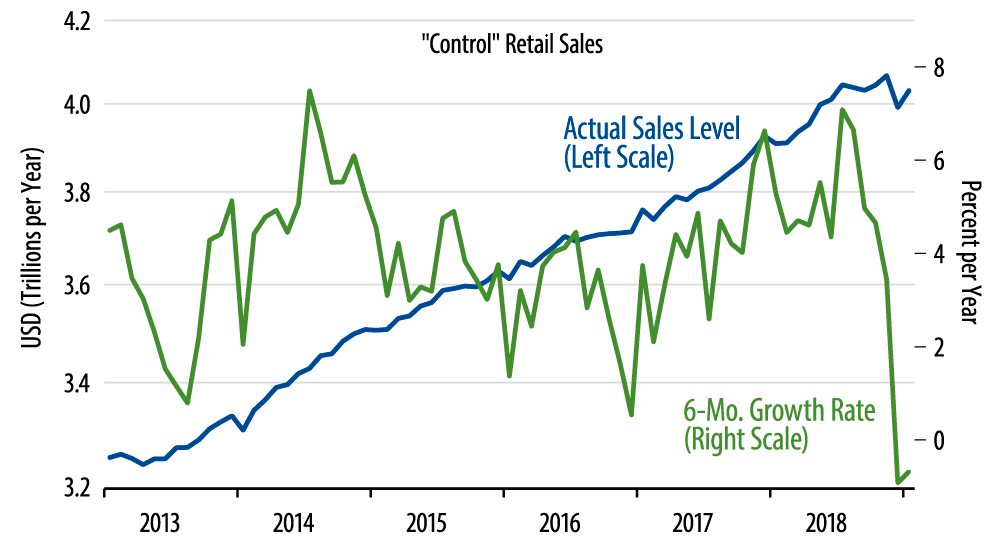

The accompanying chart shows control sales through all the recent ups and downs. As you can see, the announced January gains pulled sales levels then about back to their October level, preceding all the holiday seasons shenanigans. As stated above, there is no real hint of an emerging downtrend here, but sales growth over the last six months certainly looks softer than what we saw previously.

Six months ago, we were pointing out that surprisingly strong sales growth in November 2017 and then again in May and July 2018 had proven to be one-time bursts not followed up in subsequent months. We are inclined to think the recent net softness will prove to be similarly transitory. We have said all along that personal income growth is not rapid enough to spur accelerating consumption, but neither is it weak enough to drive declining spending.

As for weather-based explanations for the recent weakness, one of the most notable sources of softness in the sales data has been "nonstore retailers," aka online vendors. It is hard to credit that polar vortex weather kept consumers off the internet, so maybe the weather explanation doesn’t have much traction. Another possible explanation is faulty data in the wake of the government shutdown. Census and other agencies have denied such effects, but the extreme recent volatility in jobs, sales, foreign trade and housing data raise our suspicions.