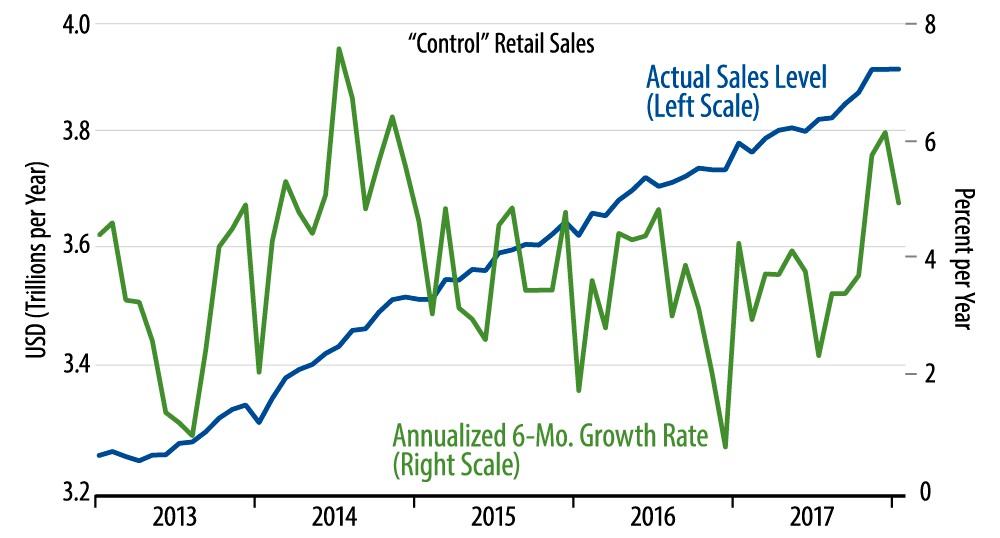

Headline retail sales declined 0.3% in January, with the November level revised down an additional 0.4%. For our "control" sales measure—sales excluding vehicles, gasoline and building materials—sales were flat in January, with December levels revised down by 0.5%. So, while most of the November "binge" was sustained in the data (only a 0.1% downward revision), consumers came back to reality with lower sales levels in both December and January.

The accompanying chart tells the story. January core sales levels are about back to the trend line that they were on in 2017 up until November. In other words, the December/January data reverse the Xmas binge.

It is the case that sales growth rates over the last six months are still elevated compared to their pace through mid-2016, but the net pace through January is off quite a bit from what looked to be in place through November. In terms of personal savings rates, the December/January declines in retail sales, thus in consumer spending on merchandise, are enough to erase the sharp dip in saving reported for November, but saving rates will still be lower in January 2018 than a year ago.

Keep in mind that the December/January softness reported for control sales does not include declines reported for motor vehicle dealers or building materials stores. With sales incentives expired, vehicle sales have dropped over the past three months back to just above summer 2017 levels. Building materials had gone flat over October-December, then declined in January.

To be clear, we are not asserting that retail sales or consumer spending are softening in any sense. Rather, through November data, the issue was whether consumer spending was spurting ahead. The answer now appears to be no: November sales seem to have been a one-time Christmas binge. Then again, that binge powered strong growth in 4Q17 domestic demand that some thought would be repeated in 1Q17 GDP data. Today’s data will probably lead many folks to mark down their 1Q17 GDP forecasts substantially.