That job growth has downshifted this year is old news. It was behind the Federal Reserve’s decision early this year to cease hiking short rates and actually to begin to cut them this summer. Naturally, with slower growth, the Chicken Littles out there are warning of recession. The fact that job growth looks to have stabilized in recent months, rather than continuing to deteriorate, should provide a second thought to the recession narrative.

Again, based on current data, growth has downshifted, but it does not appear to be on a continuing slide to actual weakness. Many analysts would claim that recent job gains are merely in line with a full employment economy. While we have mixed thoughts about that perspective, it does underline the fact that we are not seeing a continuing slide in growth such as would be consistent with the recession story.

Keep in mind that the Bureau of Labor Statistics has announced that come February it will revise the 2018 job gains down by about 40,000 per month. Meanwhile, the same source data that give rise to the coming downward revisions to 2018 growth suggest that early-2019 job growth is stronger than what the current data suggest. So, even the appearance of a 2019 deceleration in job growth may be an illusion due to preliminary, incomplete data.

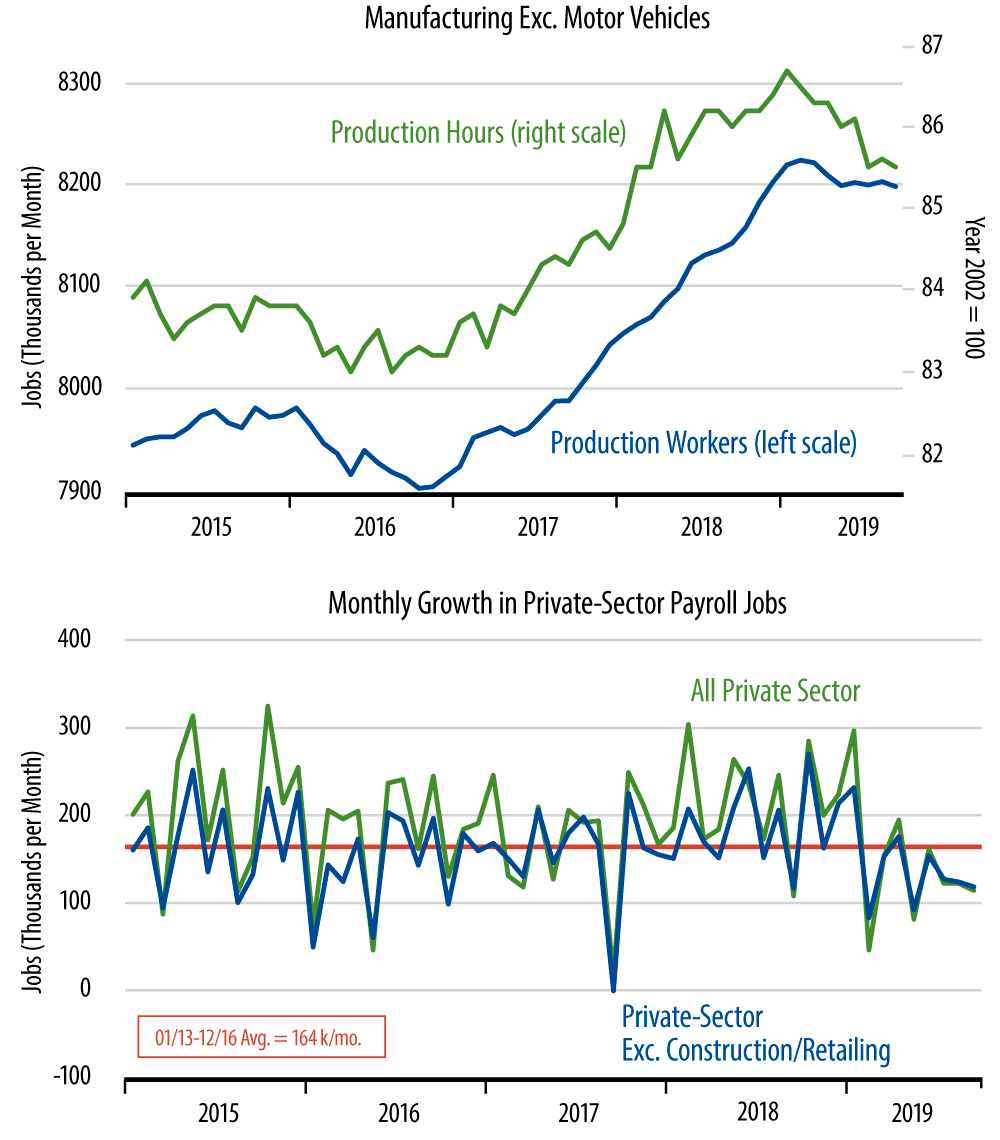

Meanwhile, the recession chant has gained some ammunition from recent readings below 50% on the Institute for Supply Manufacturing (ISM) index for manufacturing. We have never been impressed by the readings from this index. Presently, while the ISM index suggests weakness in manufacturing setting in during August and September, the hard data for manufacturing—production payrolls, production hours worked, orders, shipments and output—all showed weakness emerging in late-2018. And, if anything, this weakness of the last year has moderated in ALL the hard data indicators for manufacturing (cf. second chart here). So, for manufacturing as well as for the economy as a whole, the recession story looks way off the mark to us at this time.