Thus, private-sector payroll jobs rose by 131,000 in October. This was actually a bit of an improvement from what had been reported for the previous two months (122,000 for August and 113,000 for September), so even with the strike effects included, the headline number wasn’t bad. It looked even better when substantial upward revisions were folded in, with August and September now showing 146,000 and 149,000 gains, respectively. Finally, add back the apparent 40,000 jobs lost (temporarily) to the auto strike, and the gain in total private-sector jobs was a nice 171,000.

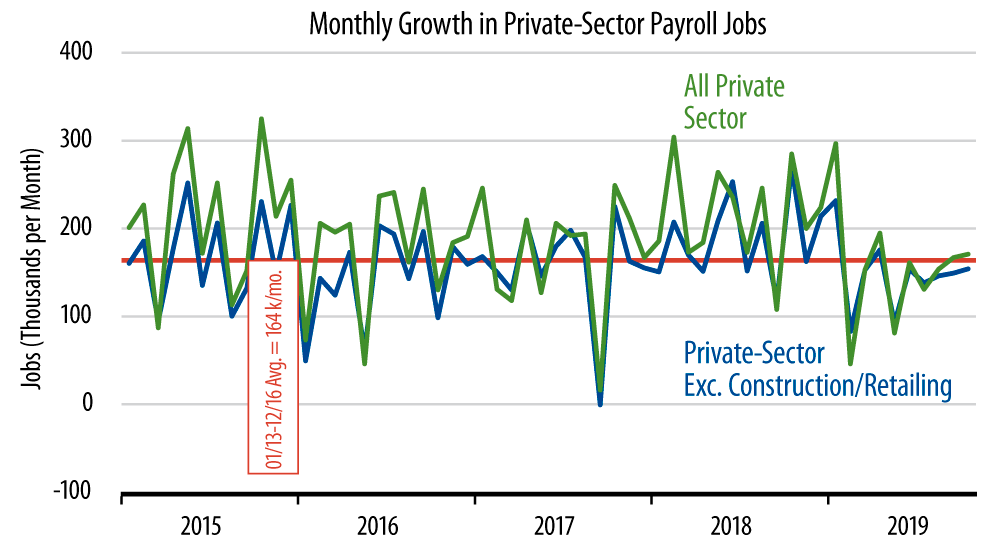

From past installments of this blog, you know that we track a "core" payroll jobs measure that abstracts from volatile construction and retailing sectors (as well as labor strikes: telecomm in 2016 and autos last month). This measure showed a gain of 154,000 in October, with August now at 146,000 and September at 149,000.

If all these strike adjustments and revision effects are spinning your head, just have a look at the accompanying chart, which tallies all these. The chart shows that recent job growth is stable or increasing very slightly, at a pace just below the average for recent years.

Keep in mind also that while 2019 job growth looks slower than that for 2018, the BLS has already announced that the 2018 gains will be revised downward by about 40,000 per month. All in all, then, the aggregate job growth picture looks decent, quite a bit better than what this same chart suggested just a month ago and not at all in line with a recession story.

Within the aggregates, factory sector payroll data also looked better ... once one abstracts from the auto strike. That is, outside of the motor vehicle sector, total factory payroll jobs have been increasing steadily throughout this year and logged a 6,000 increase in October. Factory production jobs ex vehicles have been stable for the last five months, after declining over March-May. So, the "hard" data for the manufacturing sector continue to look notably better than what the "soft data" (ISM surveys) have been indicating.