Both these gains are well below those registered for November—even after revisions—and somewhat below the average gains for all of 2019. Then again, we were coming off very strong gains in November, when, even allowing for the effects of the end of the GM strike and including today’s revisions, the gains were 203,000 for total private-sector jobs and 215,000 for our preferred measure.

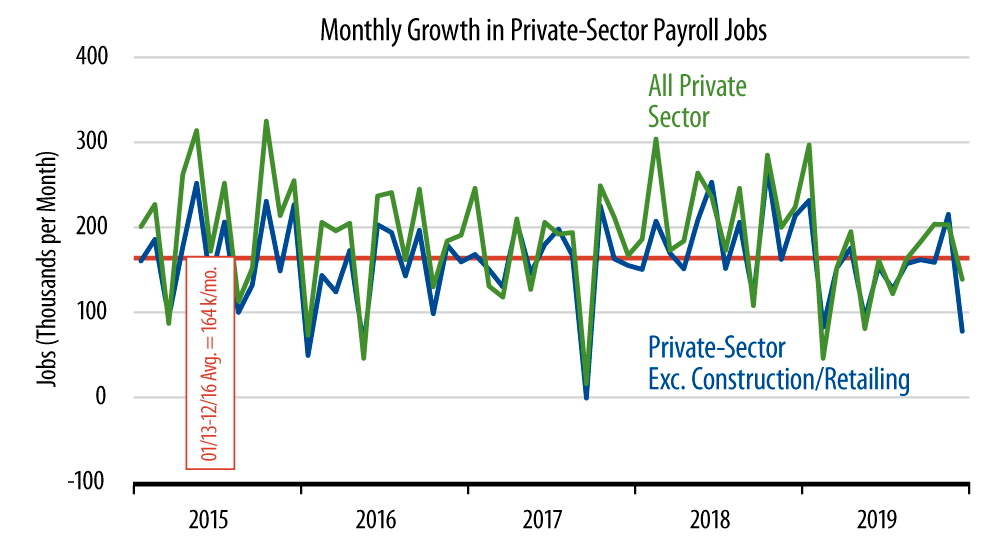

As you can see from the accompanying chart, monthly job growth rates were quite erratic in 2019, with very strong gains regularly followed by soft ones, and vice versa. For all 12 months of 2019, total private-sector jobs rose by 1.947 million, or 162,000 per month. Our preferred measure rose by 1.797 million, or 150,000 per month. Both those average gains were below the averages for 2018, 215,000 per month and 189,000 per month for the total and "preferred" measures, respectively.

Keep in mind that these slowings from 2018 averages to 2019 averages are of about the same magnitude as the downward revisions to 2018 growth that the Bureau of Labor Statistics has announced will be incorporated into the 2018 data next month, when annual benchmark revisions are released. In other words, when those revisions are in place, it is likely that 2019 average job growth will be little different from that of 2018. So, any claims that job growth slowed markedly in 2019 are consistent with the current data, but will likely prove to be incorrect just a month from now.

You might be saying, "Well, won’t 2019 data also be revised, possibly downward just as much as 2018?" The answer is yes, possibly, but most probably not. First, the revisions to be announced next month will extend only through March 2019. Second, "companion" revisions to the personal income data, based on the same source data that will be used to revise the payroll jobs estimates, suggest that job growth will actually be revised up in the first half of 2019. We’ll discuss the details of these revisions in this space in one month.

For now, job growth ended 2019 on a soft note, but the overall performance for the year was reasonably good. Economic growth in total slowed enough in 2019 to get the Fed from tightening to easing mode, but not enough to engender any serious threats of actual weakness. And the brunt of the slowing in output growth occurred in manufacturing, with likely little effect on jobs and income and no ostensible damage to the consumer sector.