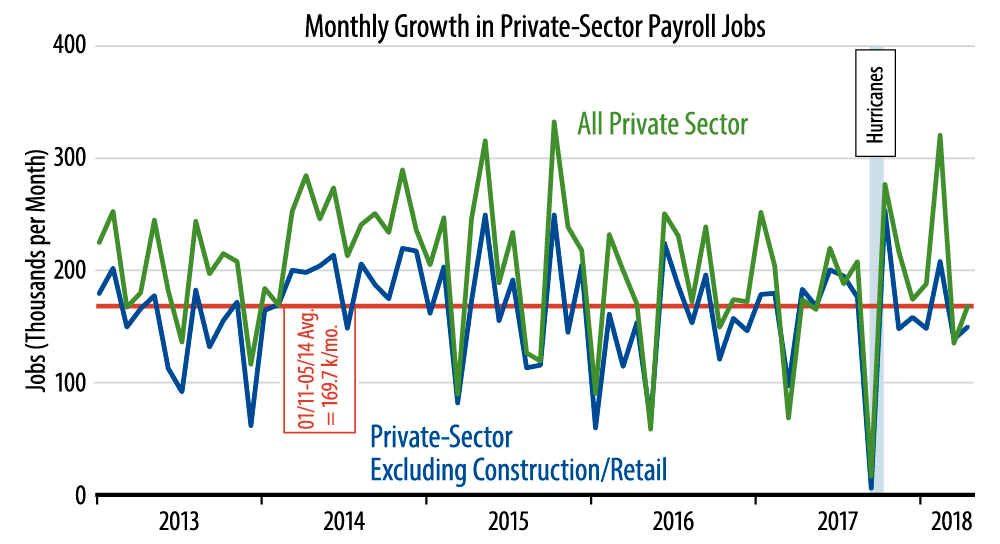

As the accompanying chart makes clear, job gains over the last eight months have generally been mediocre to soft, the exceptions being October, "payback" from a hurricane-depressed September print, and February, when modestly above-average growth in underlying job growth was boosted by huge gains in construction and retailing.

Last week, we talked about the "saga" of 1Q18 GDP growth, from the gushing 5%+ growth estimates circulating in February to the much slower estimates that resulted when actual 1Q18 data started coming in. The jobs data are a saga all their own ... or is it a soap opera?

Again, construction and retailing added 110,000 jobs in February, a month when before seasonal adjustment, jobs in those sectors actually declined by -328,000. We thought those reported February gains were a seasonal blip that would be subsequently reversed. That has not happened, as both construction and retailing have gone flat over the last two months. Then again, "flat" means the big February gains did not continue in March or April, which is why the headline jobs gains in those months have disappointed the consensus estimates.

If this is not enough "high drama" for you, move on to hourly wage data. There, we saw December and January spikes in all-worker hourly wages. However, wage gains then were only slight for "nonsupervisory" or production workers, folks actually punching a time clock. So, all the apparent "wage inflation" then was occurring among managerial staff. Well, in the three months since then, wage gains for managerial staff have come all the way back down to where they are now growing slower on a year-over-year basis than production-worker wages.

The daytime soaps would be hard-pressed to rival the dramatic twists seen in these data recently. Beneath all the sound and fury, however, not much has changed. Whether or not we are at full employment, actual job growth has been slowing, which is not consistent with the contention that overall economic growth is accelerating. Similarly, underlying wage growth remains steady and modest.