2014年7月03日時点

No doubt about it, today's payroll jobs report was a strong one. Where we differ from the market consensus is that we describe it as the first net strong report in some time. The market's take is that it is the latest in a string of strong reports.

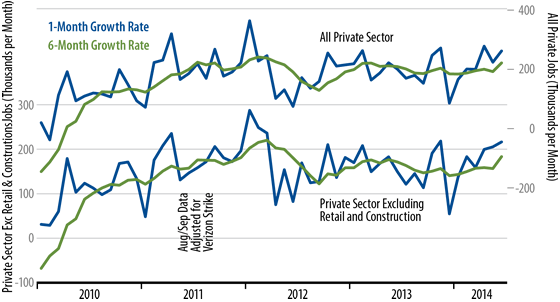

All the above 200,000 gains of previous months were needed just to offset the softness of December and January. As seen in the accompanying chart, on a six-month average basis (green lines), private-sector job growth had merely been treading water through May before finally heading higher in June. Note that this is true both for total private-sector jobs and for the less volatile "core" measure (excluding construction and retailing) that we track more closely. It took the gains of February through May just to offset soft prints for the winter months.

So, the 262,000 June gain in private-sector payrolls is a first step back toward better job trends. Still, even the one-month growth numbers for June (blue lines) show less-than-spectacular growth. And after the hole dug in first quarter—1Q14 GDP growth currently at -2.9%—the data have a lot of catching up to do to be consistent with the 3%+ GDP forecasts from the Federal Reserve. And these numbers do bounce around a lot.

The financial markets trade on a day-to-day basis. Today's news will likely be reflected in bond and stock prices over the next few days. Still, we are inclined to take a longer-term view and wait for things to average out. There has been no affirmation of net strengthening in demand indicators such as retail sales, capital orders, exports, or housing. We'll see whether the better recent job data can be sustained.