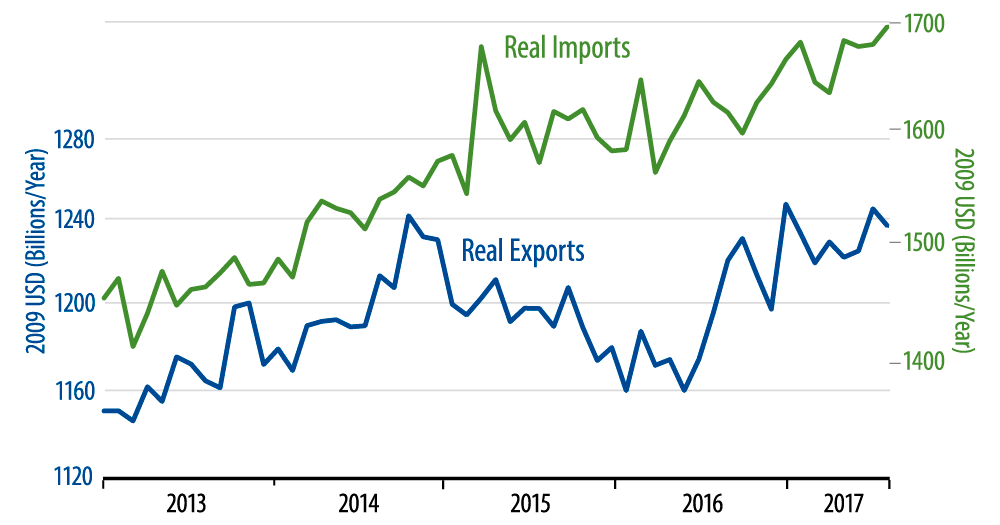

All in all, these data are consistent with previous foreign trade data for 2017, which have shown basic exports holding essentially flat. Imports are moving up more perceptibly, though even here, the growth rate is noticeably slower than was the case three to four years ago.

Sharp, sudden increases in exports last summer helped drive a second half 2016 rebound in US manufacturing output. (The other contributor was a comparable bounce in capital goods production.) Early this year, both exports and capital goods looked to be stalling, which suggested that the factory upturn would be short-lived.

Since then, while capital goods activity has resumed its uptrend, exports have continued flat. However, you wouldn’t know it from recent factory production data. Industrial production within manufacturing grew nicely in July, and the factory payroll data released last week suggest even stronger factory sector growth in August.

So, despite no growth in basic exports and despite no acceleration in consumer (or government) spending on manufactured goods, factory sector production continues on a better pace, thanks apparently to better capital spending here and abroad, as well as a faster pace of inventory accumulation.

As mentioned last week, the better factory sector growth is driving somewhat better overall economic growth in 2017 than we expected to be the case. We might grouse about the narrow range of factors driving this better growth, but it is nevertheless showing up in bottom line (top line?) growth data. Meanwhile, again, basic exports have not been contributing to this better pace, but neither have they been a big drag.