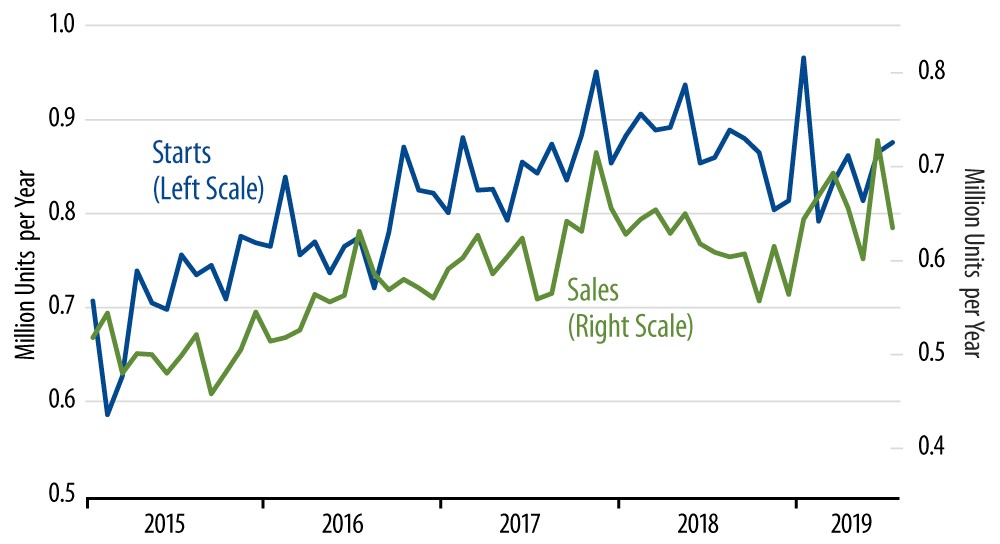

A look at new-home sales (green line) in the accompanying chart does not show the weakness one would expect from the harsh-sounding -12.8% July decline. Rather, the picture for homebuilding is much as we have described it throughout this year. Homebuilding (single-family housing starts) has declined in response to an inventory overhang, but underlying demand for new homes has held up reasonably well, enough so to think that homebuilding will stabilize once the inventory overhang has been remedied. Even with the announced July decline, new-home sales levels look largely flat—but volatile—around an underlying level of 650,000 per year.

So, what about inventories of unsold homes? They rose further in July, such that inventories of unsold new homes now stand at 6.4 months’ worth of sales. This is down from 7.4 months at the start of the year, but is still well above "normal" (sustainable?) levels of around 4 months’ worth of sales. Inventories of completed new homes rose most noticeably, while inventories of unsold homes under construction declined.

So, the overhang of unsold homes is most glaring among completed homes, exactly where they tie up the most (idle) capital for homebuilders and so exactly where they are most an issue for builders. As before, we expect housing starts and construction levels to continue to decline until inventories of unsold homes have dropped substantially from current levels. This will take further, sustained declines in housing start levels and would seem at present to take another three to six months.

While we expect further declines in homebuilding, we don’t foresee a prolonged, tumultuous decline such as occurred over 2006-09. Besides the generally flat trend for new-home sales overall, the regional new-home sales data also support this contention. That is, the South accounts for over half of all US homebuilding, and new-home sales and starts in the South continue to hold up very well, with most of the decline in starts occurring elsewhere in the US.