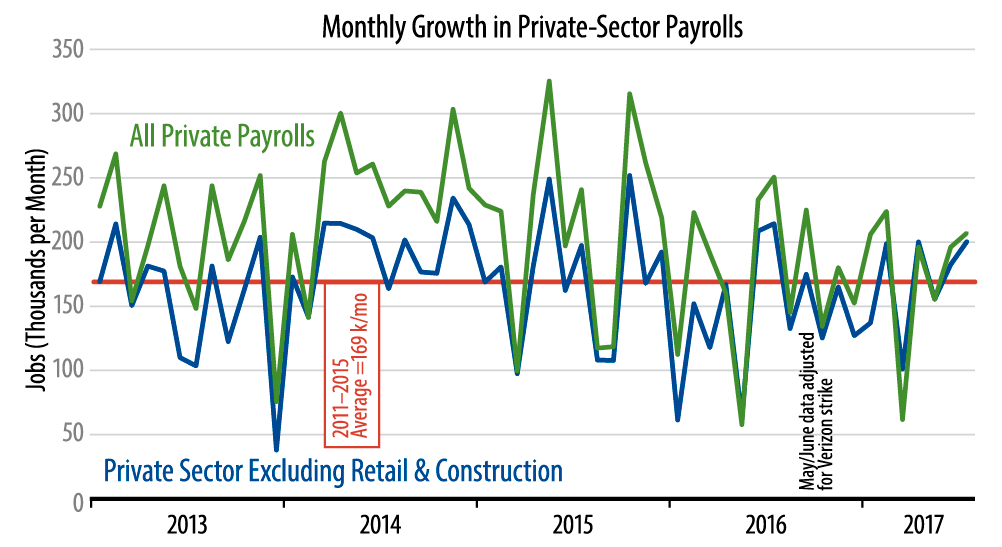

As you can see in the accompanying chart, both of the last two months’ gains are above the average growth rate for 2011–15. In contrast, over the previous 17 months, we had been below that 2011–15 average 12 times. In other words, the last two months do mark an improvement over what job growth had been for the past year or so.

Another important feature of the report, for our forecast at least, was news of good-sized job gains in the manufacturing sector. Factory jobs rose by 16,000 in July, with 17,000 job gains for factory production workers (line workers). Factory jobs had fizzled over the previous two months, after nice gains in late-2016, and our guess was that softening exports and capital spending growth would drive continued softness in manufacturing activity in late-2017. The July news was at odds with this outlook.

Hourly wages rose by 0.3% in July, both for production workers and for all workers. Even with this better growth, however, the 12-month growth rates in hourly wages for these aggregates, at 2.5% for all workers and 2.4% for production workers, are down noticeably from what we were seeing in 2016.

Where did the better job growth occur? The really noticeable improvement was in leisure and hospitality (restaurants, hotels and resorts), where recent average job gains have been 45,000 per month, compared to 20,000 per month gains earlier this year.

One month does not make a trend, nor even do two months. Still, we have to acknowledge that overall job growth has been better in the last two months than we were expecting, and factory jobs were better in July. Another stronger gain in August would put our forecast line in jeopardy. It would also substantially raise the chances for a Fed rate hike in September.