2015年08月07日時点

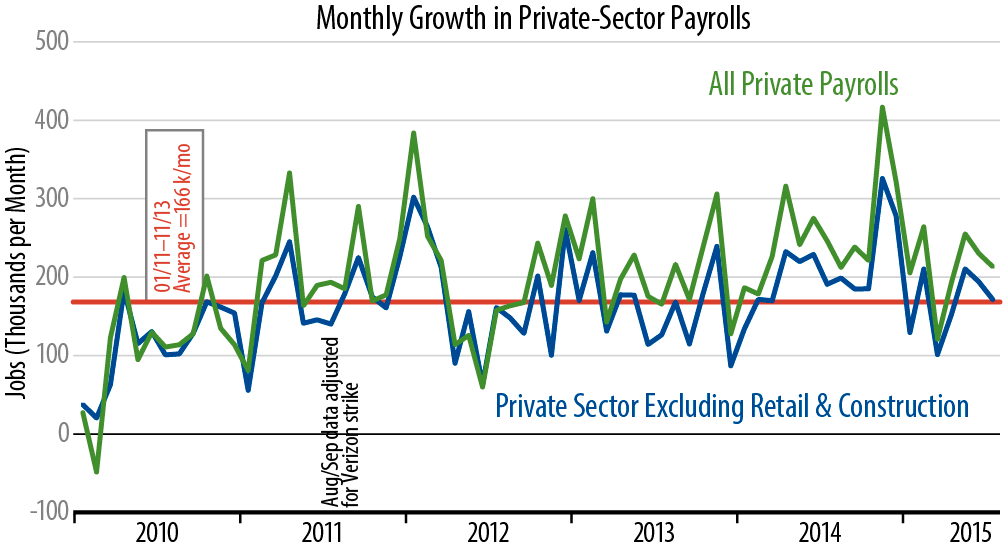

Private-sector payrolls rose 210,000 in July, with our “core” measure (excluding construction and retailing) up 168,000. June data saw minor revisions: total private sector revised up 6,000, core payrolls revised down 1,000. The gains were in line with expectations, and as seen in the chart, they were also in line with the trend growth rates of the last 5 years.

Therein lies the rub. Those who say that the economy is doing fine will cite these numbers in support of their story. Those who worry about the sluggish growth pace of recent years will also find support in today’s data.

Wall Street consensus analysts—and some Fed officials—have been trying to have it both ways. They have been extolling recent job growth rates, while also extolling “improvement” in the economy... which sure sounds like accelerating growth. Today’s data—as well as those of recent months—clearly do NOT indicate accelerating growth, so the Street and Fed take is at best only half right.

Is “half right” enough to drive a 2015 rate hike? Probably. If nothing else, it would be extremely hard and politically delicate to initiate rate hikes in the middle of a 2016 presidential election campaign, so the economy would have to deteriorate markedly to clearly forestall Fed action this year.

That hasn’t happened. While GDP growth has slowed so far this year, job growth hasn’t. So, a rate hike is on the table, but to our minds, the more important question is whether the Fed will hike rates aggressively enough to push down stock and bond prices. We don’t think the Fed wants that.

In other aspects of the report, the unemployment rate held steady, but the employment rate (jobs divided by adult population) weakened. We are still at a lower employment rate now than was the case at the trough of the recession in June 2009. Within the manufacturing sector, jobs rose in July, but that gain was fully offset by downward revisions to July data, so the 2015 factory stall looks to still be in place.