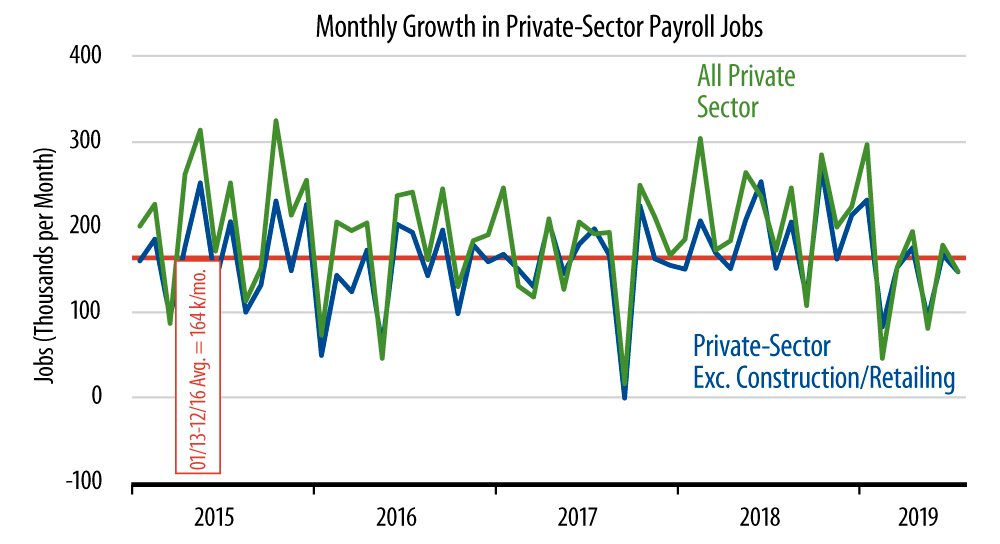

The data are summarized in the accompanying chart. As seen there, private-sector job growth has been lower throughout the last six months than what it registered over most of 2018, and it has also been slightly below the prevailing rate of the last five years (red line in chart).

The bulk of this slowdown is due to a year-long slump in manufacturing. We are bemused by all the current talk about factory sector slowing, as if this were a very recent development. In fact, factory payroll data have been softening since January, and data on factory orders and production indicate a slowing that actually began in August 2018.

We emphasize this because the recent data hint at the beginnings of a rebound in US manufacturing, a point lost on many commentators. Factory production worker job losses slowed to a dribble in May and June, and today’s data showed a strong gain of 21,000 manufacturing production-worker jobs, alongside a slight, -0.1 hour decline in production-worker average workweeks.

Granted, total factory payrolls rose "only" +16,000, and all-worker factory workweeks dropped by -0.3 hours. In other words, production-worker payroll data for the factory sector were much stronger than the corresponding overall factory payroll data. What this suggests is that after 11 months of a production "stall," manufacturers are still cutting back on back-office help, but they appear to be beginning to ramp up production schedules again. This rebound is still tentative in the data, but it is a positive sign that many seem to have missed.

Meanwhile, hourly wage gains were modest. Our take is that wage growth has stabilized in 2019 at an annual rate right around 3.0%. This is slower than the 3.5% gains seen in 2018, but is still an improvement from the generally 2.5% growth over 2015-17 and is sufficient to drive continued decent growth in consumer spending.

All in all, overall job gains were slightly soggy but steady, and we are encouraged by the tentative signs of rebound that the manufacturing sector is showing.