2015年08月13日時点

Retail sales showed decent growth in July, with headline sales up 0.6% and the control measure we track up 0.3%. In addition, June growth in control sales was revised upward, from -0.1% to 0.2%.

Much of the strength in headline sales came from a 1.4% increase in car sales, but that merely offset a 1.4% June decline. On net, car sales have shown steady growth for the last five years. Elsewhere, things have been more fitful. Sales at furniture and book/sporting goods/music stores have grown nicely recently, while sales at electronics stores have declined, and sales at grocery and department stores have flatlined.

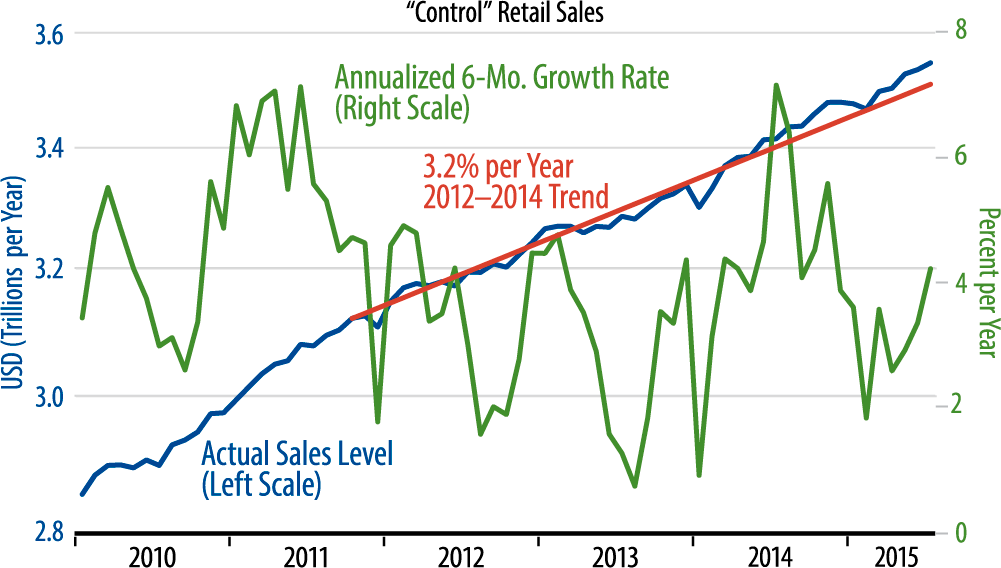

The 0.2% to 0.3% recent gains in control sales are indicative of retail in general: decent but not spectacular and no real change from the modest growth trends of recent years. As seen in the accompanying chart, underlying retail sales levels moved above 2012–2014 trends late last year, but since then, sales growth rates have fluctuated between 2% and 4%, about the same as in previous years.

So, it is not accurate to say that the retail sector is hurting, but neither is it providing the “jolt” upward that will propel faster overall domestic growth. Meanwhile, as we have commented in past offerings, the slower overall economic growth seen this year has been driven by substantially softer trends in capital spending (CAPEX) and exports. Those downtrends are still in place through recent data, and if indeed retail sales growth has improved this year, it has not done so enough to fully offset the drags from CAPEX and exports.

As was the case with the jobs data last week, the retail sales data are not soft enough to preclude late-2015 Federal Reserve (Fed) rate hikes, but they do suggest that the Fed’s moves will be cautious, intended to have little or no adverse impact on bond and stock prices.