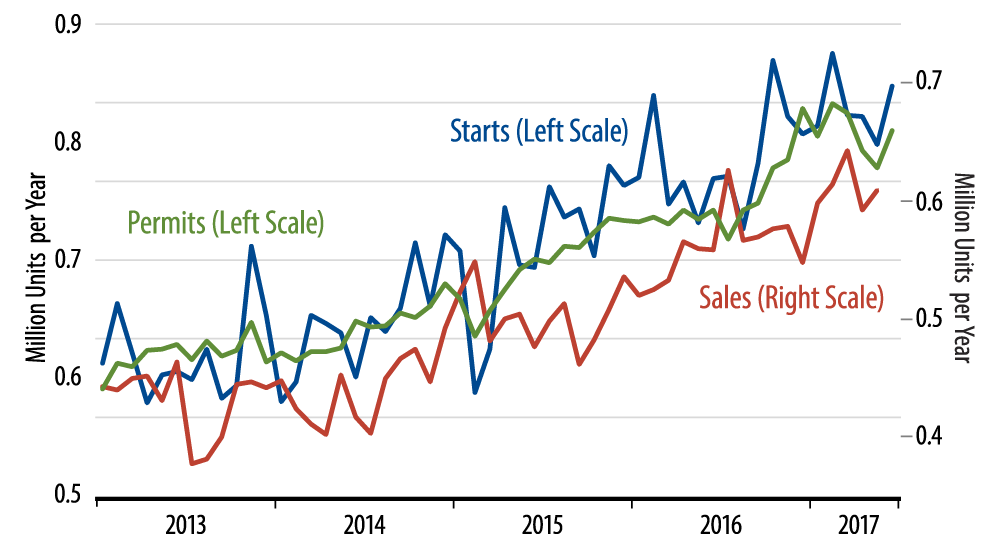

Our call has been that homebuilding activity would flatten over the rest of this year. As impressive as the June gains might sound, they are fully in line with this outlook. The starts level trend has looked flat, though volatile, ever since the October 2016 jump. Single-family permits have been similarly flat-to-down since then.

Finally, new-home sales, by our reckoning, still have not achieved levels sufficient to sustain current single-family starts levels, let alone to stimulate further gains in starts. Supporting this reckoning is the fact that unsold inventories of new homes have been steadily rising over the last nine months, indicating that, indeed, homebuilding levels exceed the pace of new-home sales.

Our focus in tracking the housing market is determining its impact on US GDP growth. From this perspective, the issue with housing, as with any other sector, is what have you done for me lately. That is, regardless of whether current housing start levels are high or not, they need to be rising if homebuilding is to contribute to GDP growth.

The spike in single-family starts last fall drove a nice increase in residential construction spending and in GDP in 4Q16 and 1Q17. However, with starts stuck in a range ever since then, residential construction spending has been topping out in recent months, and, again, today’s data suggest continued flat-lining in single-family construction, so no boost to growth from homebuilding in mid-2017 or, likely, thereafter.

Similarly, while multi-family starts rose 13.3% in June, those gains also only partially offset much larger declines over the preceding four months, so multi-family homebuilding looks to be continuing on the downtrend it has followed over the last 10 months. On both counts, then, the strong-sounding June housing starts data are quite consistent with homebuilding trends that are at best flat going forward.