2015年07月02日時点

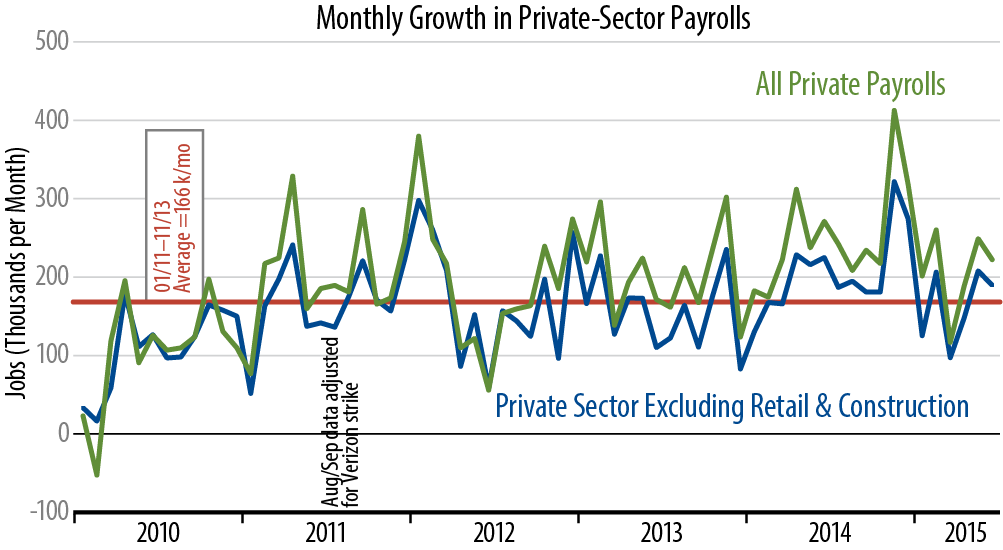

After a strong May report, payroll employment growth slowed a bit in June, with private-sector jobs up 223,000. April and May gains were revised down, from 206,000 and 262,000 to 189,000 and 250,000, respectively. All in all, job growth is not tanking, but also not accelerating.

As the chart makes clear, job growth continues to meander around the trend rate of the last five years. The very strong gains of November and December were an aberration, as were the especially soft gains of January and March.

While job growth has continued steadily, GDP growth has sagged this year. With 1Q15 GDP growth still negative and 2Q15 likely to be around 2%, the first-half average rate will come in at only 1%. The reason GDP growth has sagged alongside steady job growth lies with the US manufacturing sector. Factories don’t generate a lot of job growth, but they do account for most of the swings up and down in GDP growth.

So far this year, factory-sector growth has stalled, depressed by declining capital spending and exports. Today’s payroll report did not show any meaningful improvement in factory jobs or workweeks in June. This suggests that the 2015 factory swoon was still in place through mid-year and with it, slower GDP growth as well.

The combination of steady job growth but softer GDP growth makes the timing of Fed rate moves uncertain. The Fed may cite the jobs data and move in September, or it may hold off due to ongoing softer growth in GDP. If the Fed does move, it will likely do so very cautiously, attempting not to move the markets much. This last consideration is probably more important than whether or not the Fed does move this year.