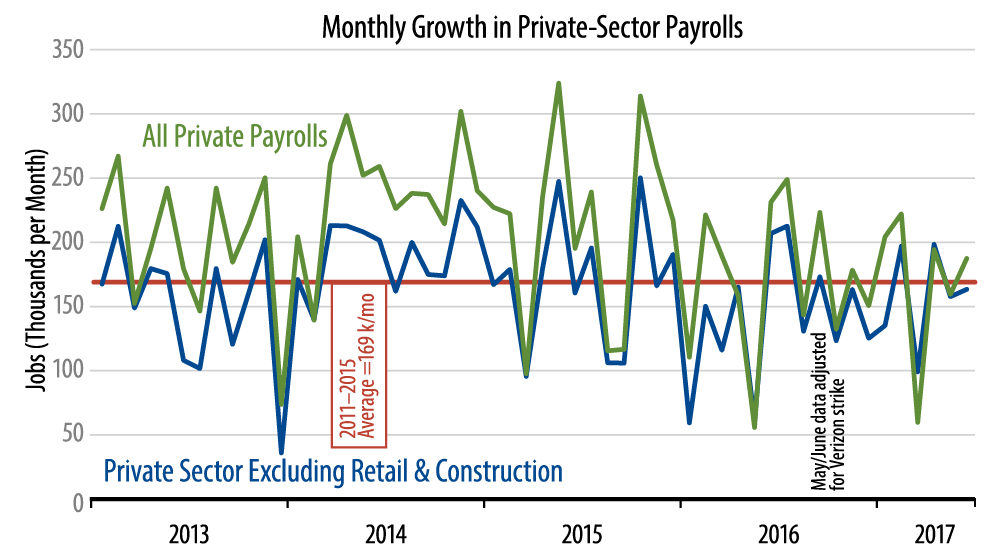

The chart puts things in context. Though core job growth picked up slightly in June (blue line), that growth was still slightly below the 169,000 per month average growth rate for 2011–15. Nine out of the last 12 and 13 out of the last 18 months have seen growth below this average.

As we have remarked previously, the consensus view is that even though job growth is slowing, this is just fine, because the economy is at full employment. However, slower job and wage growth mean slower income growth, which precludes any pick-up in consumer spending or in the economy. So, even if the economy is at full employment, it is not currently “improving.”

That core job growth lagged the headlines indicates that job gains were stronger in government, retailing, and construction. The retailing gains were 8,000 in June, following losses of 80,000 over the previous four months. Construction saw gains of 16,000 in June, after cumulative gains of only 9,000 over the preceding three months. Similarly, the 35,000 June gain in local government jobs follows cumulative gains of 16,000 over the preceding eight months. So, while all three of these sectors saw improvement in June, each of these can be described as spurious, especially with June seasonal factors—the move to year-round schooling—possibly distorting local government jobs.

Meanwhile, hourly wages were up less than 0.2%, bringing their 12-month growth rate to 2.4%, down from 2.8% just six months ago. Factory production jobs declined in June for the second straight month, so it looks as though the factory rebound that began last fall has fizzled.

So, yes, the June job data were better, but they pose no challenge to our contention that the economy is slowing again, likely enough to stay the Fed’s hand on rate hikes.