2015年07月14日時点

Retail sales were reported as declining in June, alongside slight downward revisions to April and May. Thus, retail data have reverted to the same old soggy trends in place for most of the last six months (and six years), with those trends interrupted only by a more upbeat release a month ago.

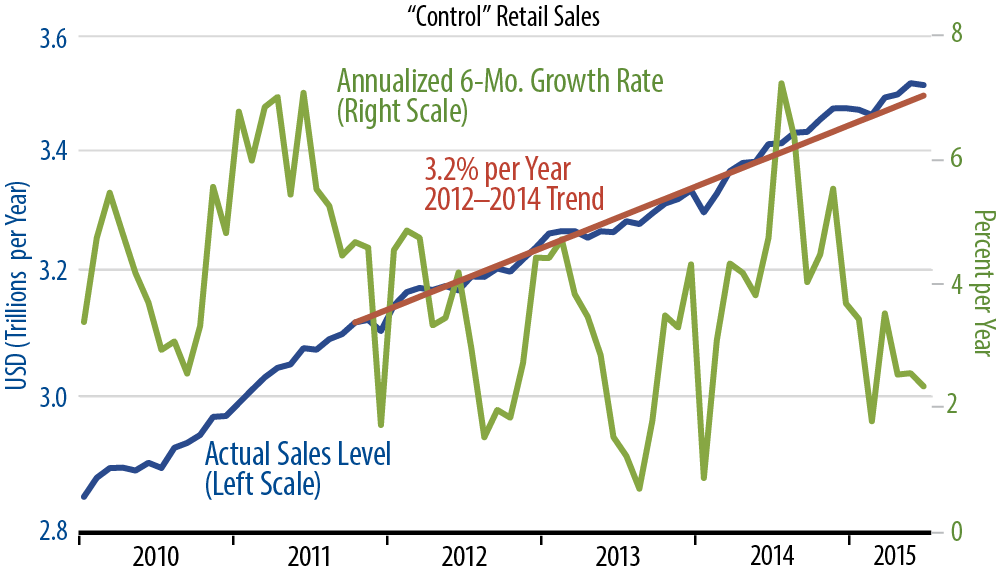

The accompanying chart shows our measure of control retail sales (which differs from others’ in that we include restaurant sales). This measure declined 0.1% in June, and the May gain was revised down to 0.6%. Control sales rose at a 2.4% annualized rate over the first half of 2015, with headline (total) sales up at a 2.0% rate. Both rates of increase are below the trend growth rate of recent years. In the chart, you can see control sales in June essentially back on the 2012–2014 trend path, following a slight, temporary move above trend in late-2014.

Our attention has been more focused on ongoing softness in capital spending and exports, which we believe have been the main drivers behind the 2015 stall in US manufacturing activity, thus also the main driver of slower GDP growth in the first half of 2015. However, the retail sales data are right in line with this story. There has been nothing within consumer spending to offset the slower growth in capital spending and exports, so that overall growth has moved lower, from a 2.0%–2.5% trend over 2010–14 to something like 1.0%–1.5% growth so far this year.

Hopes were raised last month when the June data releases came in generally stronger than preceding months. However, jobs, exports, and now retail sales have all come in soft in July, reverting to the trends in place prior to last month’s news and making the June news look like a blip.