2014年7月15日時点

Today's retail sales data were very much like the jobs data 12 days ago: while the monthly gains and revisions have been favorable, this latest release was really the first bit of good news in quite a few months. With the jobs data, we needed above-trend gains over February through May just to offset the winter weakness, so the above-trend gains in June were the first net positive in a bit more than a year. With retail sales, the gains over spring were so tepid that we needed today's upward revisions and June gains merely to offset the winter weakness. So, there is now no longer any real indication of a net slowing in retail sales this year, but neither is there any net improvement.

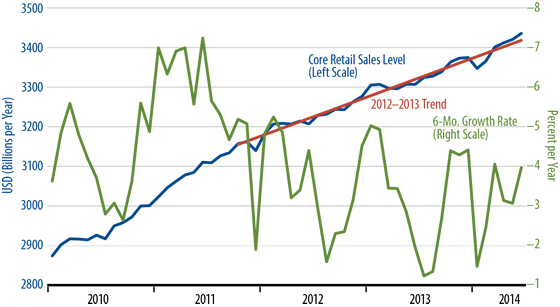

The chart tells the story. Looking at the "core" or "control" measure of retail sales, you can see the monthly data on the blue line versus a continuation of 2012–13 trends depicted by the red line. Clearly, recent sales numbers are barely above-trend after the January-February data fell well below trend. If you tote up the deviations relative to trend over the last six months, you find that sales for 2014 to date are on average right in line with—actually, very slightly below—previous trends.

The bottom line for the overall economy is that we need a net acceleration somewhere to drive the 3% or so GDP growth that the Federal Reserve and most Wall Street analysts are projecting. We don't have such an acceleration in retail sales or consumer spending in general, nor have we seen it in other sectors such as capital spending, housing, exports, or government outlays.

Looking more closely at the details of today's retail data, sales were actually softer in the items the control measure excludes: motor vehicles and building materials. In fact, while we stated at the outset that the headline data were favorable, the fact is that virtually all the strength in today's news was concentrated in the warehouse/club store category. These stores saw an especially soft winter, but sales there have ramped back up in recent months.