Baseline retail sales showed nice growth in June, following more robust gains in April and May. Our “control” measure of retail sales was up 0.35% in June, following gains of 0.46% in May and 0.91% in April. The headline retail measure showed a gain of 0.57% in June, but that was partially offset by -0.26% of revisions to May data. (The control sales measure for May saw essentially no revision.)

Why were headline sales up more sharply? Two reasons: higher gas prices and a rebound in building materials store sales following earlier weakness. Thus, sales at service stations rose 1.1%, in line with the recent bounce in gas prices. Sales at building materials stores rose 3.9% in June, on the heels of a 4.5% decline over March–May.

The control sales measure abstracts from these sectors partly because they are not as consumer-focused as other sectors and partly because of their extreme short-term volatility. The latter was certainly apparent for these sectors in recent months. For the other sector excluded from control sales, motor vehicle dealers, sales were up a scant 0.06%, which made only a slight dent in the 1.5% decline registered over the preceding 5 months.

It continues to be the case that the bulk of the recent improvement in sales growth has gone to online retailers (up another 1.1% in June). For traditional, brick-and-mortar retail sectors, department and apparel store sales continued flat. Restaurant sales growth has slowed recently, while grocery store sales have picked up. Furniture and electronics/appliance store sales continue sluggish, while sales at books/sporting goods have grown nicely.

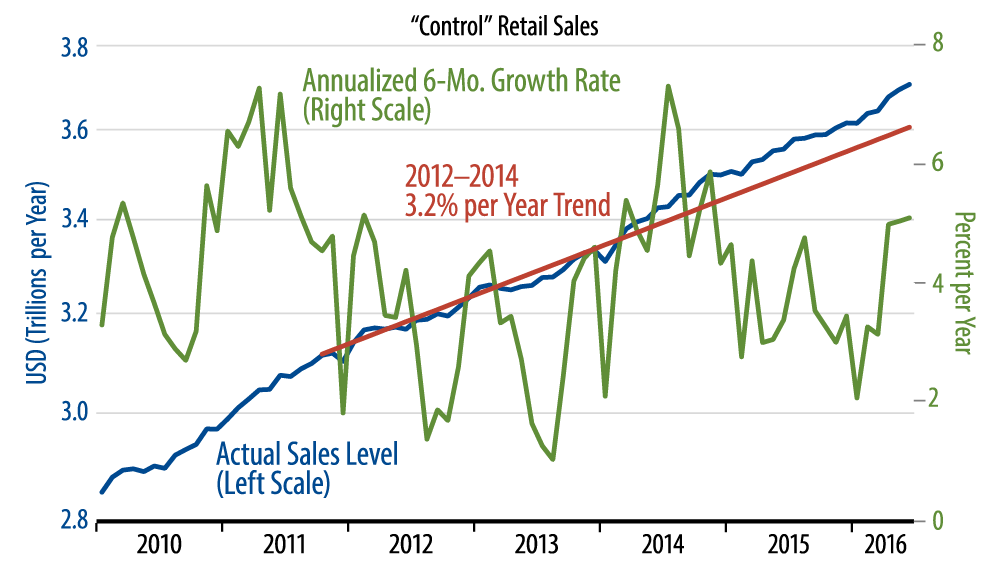

Looking through all the clutter and chop, underlying retail sales growth has improved over the last three months, as is clear in the accompanying chart. The gains aren’t large enough to single-handedly drive robust GDP growth, but they have been enough to dampen recession fears. We perceive the news to be consistent with our forecast line of GDP growth in the 1.5% +/- range.