We’re told there is an old Chinese curse “May you live in interesting times.” US jobs data have certainly been interesting the last 2 months, with the May data horrible and today’s June data terrific. Average together “horrible” and “terrific,” and you still get only tepid.

Private-sector payroll jobs were up 265,000 in June, following revised changes of -6,000 and +147,000 in May and April, respectively. Net out the effects of the telecommunications strike and the gains become +32,000 in May and +227,000 in June, averaging out to a tepid 130,000.

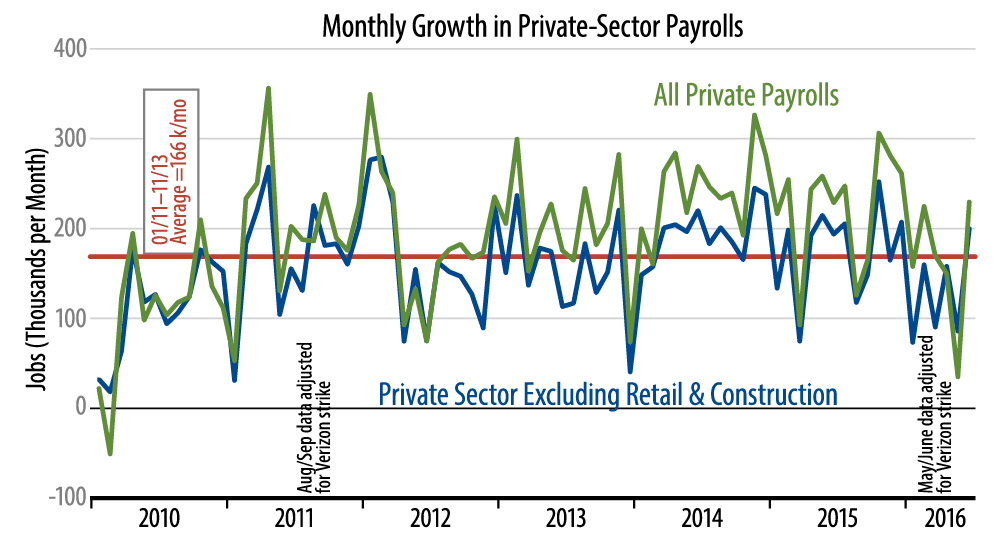

Meanwhile, the volatile construction and retailing sectors continue to retrace the outsized growth reported around the turn of the year. Between November and March, these sectors together averaged +80,000 jobs per month. Over the last 3 months, they have averaged only 3,000.

The upshot is that though headline jobs data appeared to have slowed only in the last 3 months, abstract from construction and retailing, and it is clear that the slowdown has been in place throughout 2016. As shown by the blue line in the accompanying chart, private-sector job growth net of construction and retailing broke slower starting in January 2016 and has continued thus.

This less volatile measure showed a gain of 197,000 in June, tempered by a gain of only 45,000 in May. For the first 6 months of 2016, its average growth was 119,000 per month, compared with trend gains of 166,000 per month over 2011–15. The 121,000 average gain there for the last 2 months is right in line with this slower 2016-to-date trend.

This slowing has been focused in manufacturing and its adjuncts: mining, logistics, and professional services. All these sectors have shown weak job growth throughout 2016, whereas job growth in service sectors unrelated to manufacturing has held steady. And these trends remained intact within the June data, despite its “interesting” turn.

Our guess is that this leaves the Fed on hold. Again, job growth has been slow for quite some time, the factory sector remains weak, and today’s data do not meaningfully alter this picture. Meanwhile, the added concerns arising from the Brexit vote further stay the Fed’s hand.