As seen there, June growth was stronger than what we have been seeing for most of the previous nine months. So, while the "headline" gains announced today were not as strong as those of previous months, we judge the underlying details of this report to be the strongest since summer 2017.

On the other side of the ledger, hourly wage growth moderated to a 0.2% gain in June, and the unemployment rate ticked up to 4.0% from 3.8% in May. Within the household survey that generates the unemployment rate data, labor force participation picked up, while household employment growth slowed, thus the increase in unemployment.

So, today’s news contained something for everybody—better payroll job growth for those touting a stronger economy, but higher unemployment and contained wage growth for those thinking the Federal Reserve should slow its pace of rate hikes. Our own view has been that neither economic growth nor inflation were picking up the way market sentiment has been perceiving. Today’s job growth news was not supportive of our view on growth, but we would counter that previous months’ data were not as buoyant as consensus perception had alleged.

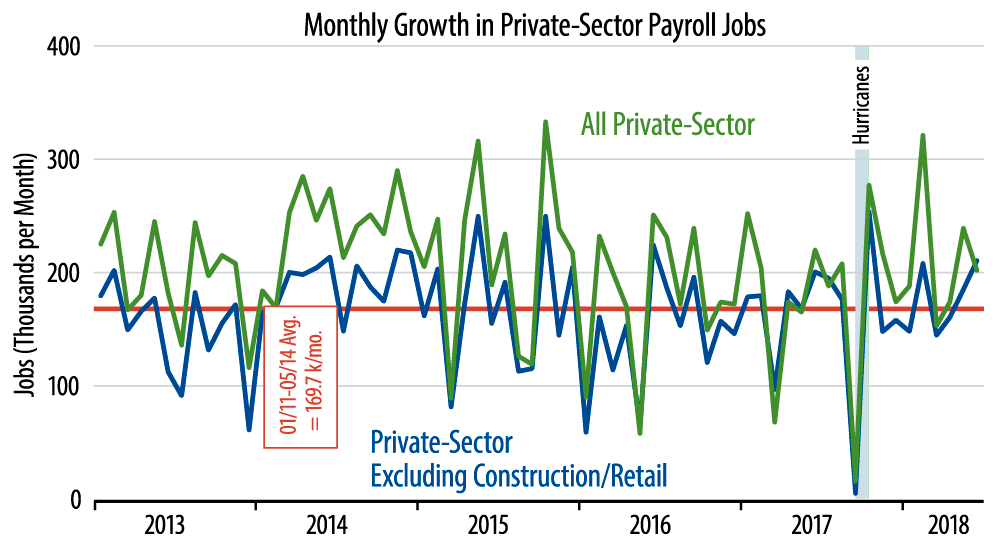

Meanwhile, again, our favored jobs measure excludes construction and retailing, because of their seasonal volatility. Both measures had jumped early in the year, and both moderated in June.

Finally, manufacturing is the one sector showing significant improvement in job growth in the last two years. The June data announced this morning continued that skein, with factory jobs up a nice 36,000, and factory production jobs up 27,000.