Recent inflation rates have been about in line with what the Federal Reserve (Fed) is looking for. However, the Fed's targets concern the core price deflator for Personal Consumption Expenditures, aka the core PCE. This indicator is calculated a bit differently from the CPI, has been running a bit cooler recently than the CPI, and likely will not show a 2% year-over-year gain for March. (Its March move will be reported on April 30.)

A notable difference between the core CPI and PCE readings is that the seasonal adjustment factors for the CPI have been recently revised. The elevated inflation readings (on a one-month basis) that the core CPI shows for January and February had also originally occurred in January/February of 2016 and 2017 . . . until new seasonal adjustment factors revised them away. So, the January/February turbulence in prices looks like a recurring phenomenon for the core PCE, but a new development for the core CPI.

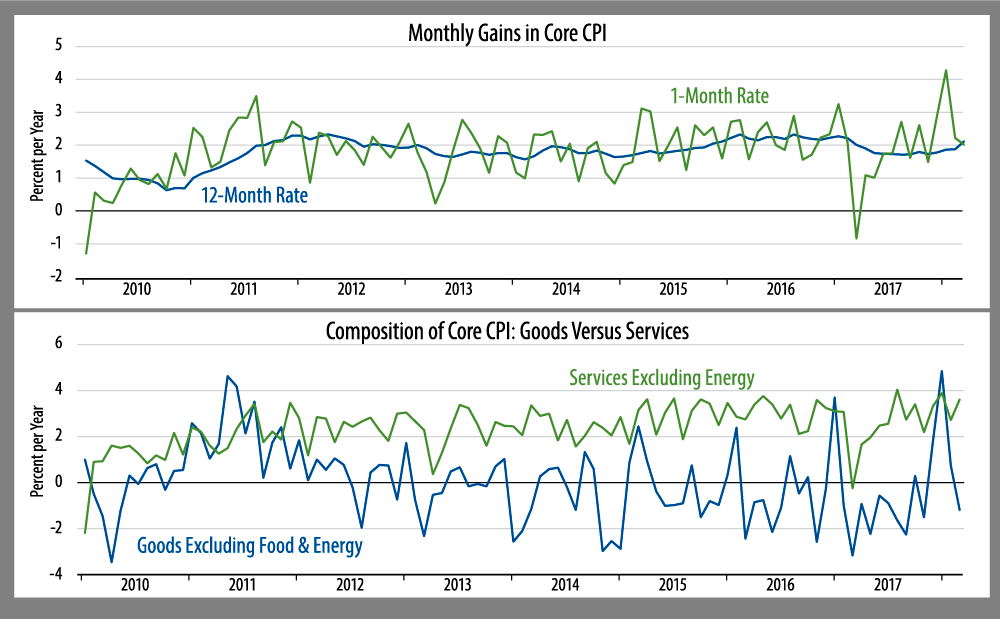

One other element of inflation that is worth noting is the disparity between goods and services prices. When analysts talk about an overheated economy, they invariably refer to services. After all, manufacturing has shown essentially zero output since 2012, and factory capacity utilization rates are very low. Yet, as the second chart shows, all that January/February turbulence was in goods prices, echoing similar bounces at this time one and two years ago. Goods prices declined in March, even excluding energy prices. Services inflation has been steady.