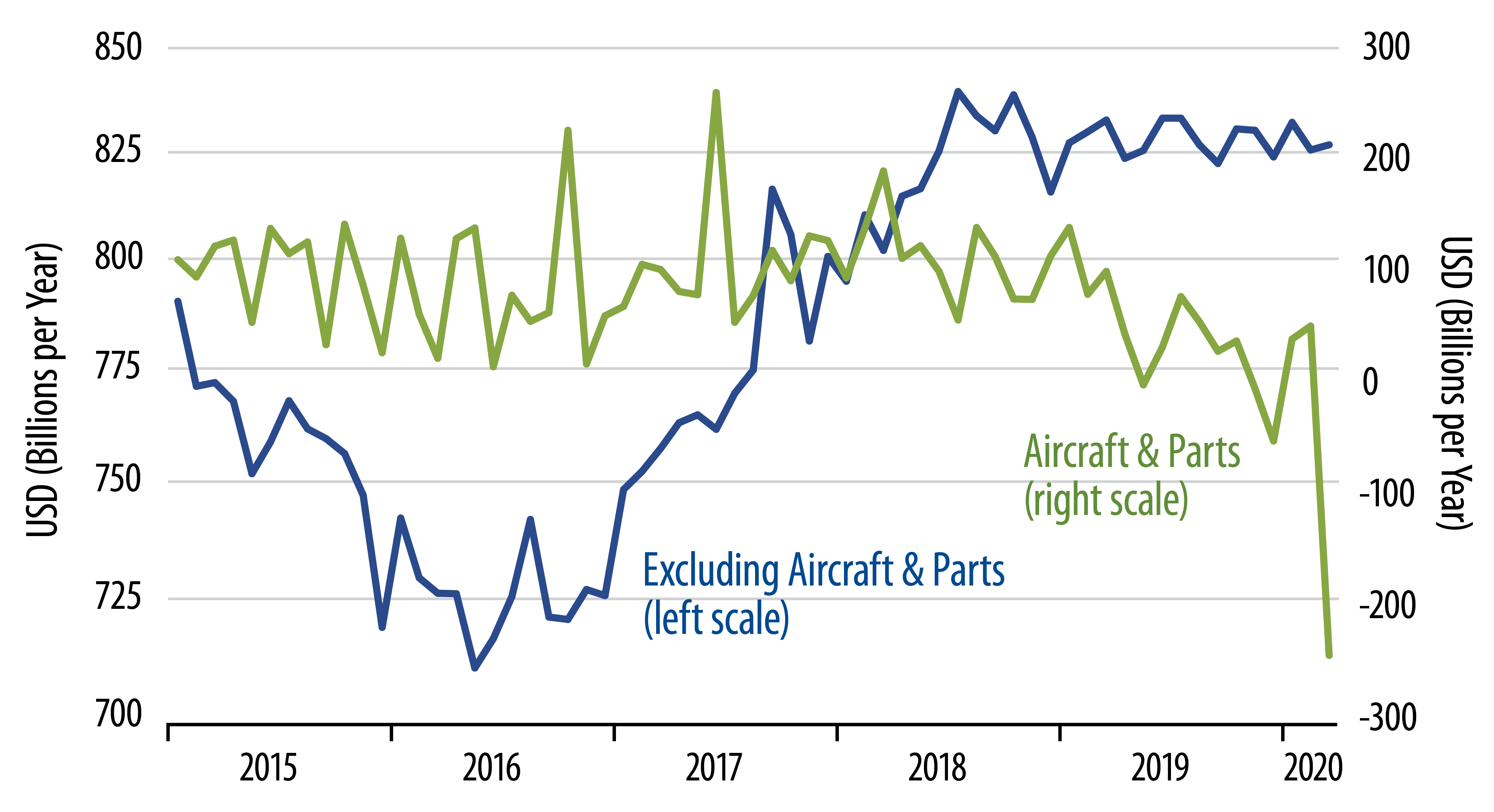

Earlier this month, we were surprised at how quickly the COVID-19 shutdown permeated the economic data, with both payroll jobs and retail sales dropping sharply in March (and even sharper declines expected for April data to be announced next month). Durable goods orders present the opposite experience. Outside of aircraft, durable goods manufacturing hummed right along, with no clear moves to the downside.

And even within aircraft, that sector was hurting from Boeing’s troubles long before the virus set in, so it is not clear how much of the March plunge is virus-related. Speaking of which, we saw negative oil prices early this week, and today we saw a substantially negative order count for aircraft. What this means is that cancellations of existing orders exceeded any new orders that may have been placed by about $20 billion, which was annualized to a -$242 billion rate.

Unfortunately, this relatively favorable performance for durable goods activity can’t last. It likely reflects orders and shipments activity booked earlier, as a wide range of factories have been subjected to the shutdowns. Furthermore, Federal Reserve (Fed) industrial production data released last week showed a -9% drop in durable goods production in March, and this decline is likely to be reflected in durables orders and shipments in April.

So, no, we are not near to being "out of the woods" with respect to virus-driven declines in the economic data. Then again, financial markets have stabilized, for now, and it appears that investors are taking a non-panicked view of things, thanks to some stabilizing activity by the Fed.

We are among those who believe the coming post-shutdown economic rebound will be stronger than many expect. So, hopefully, there is something to look forward to not too far down the road. However, we’ll have to get through another month or more of bad economic news before we can turn that corner.